Meaning of descoped for PCI: What It Means for Security and Compliance

Discover the meaning of descoped and how it affects PCI compliance, security controls, and risk management.

Read article

Compliance in financial services industry: A Practical Guide

Master compliance in financial services industry with practical steps to navigate regulations, protect data, and optimize secure payments.

Read article

What Is PCI DSS A UK Guide for Contact Centres

Confused about what is PCI DSS? This guide explains the 12 core requirements, merchant levels, and how UK contact centres can achieve lasting compliance.

Read article

PCI DSS What Is It A Plain English Guide for UK Businesses

Confused about 'PCI DSS what is'? This guide breaks down the 12 requirements, compliance levels, and how modern tech simplifies everything for UK businesses.

Read article

What Is PCI Compliant? A Practical Guide for Merchants

what is pci compliant? Learn PCI DSS basics, merchant levels, and steps UK businesses can take to secure payments and reduce scope.

Read article

Understanding Your Level of PCI Compliance in the UK

What is your required level of PCI compliance? This guide demystifies merchant levels, validation requirements, and how to reduce scope for contact centres.

Read article

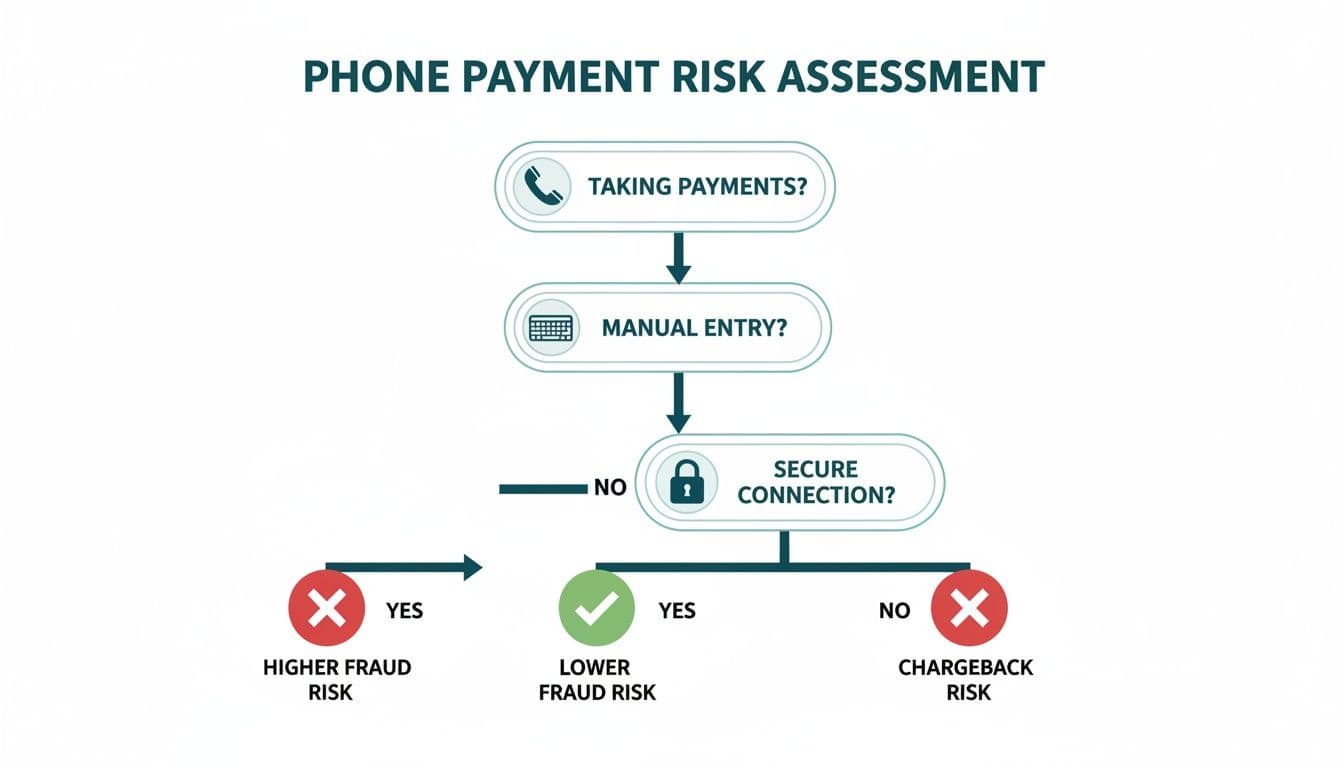

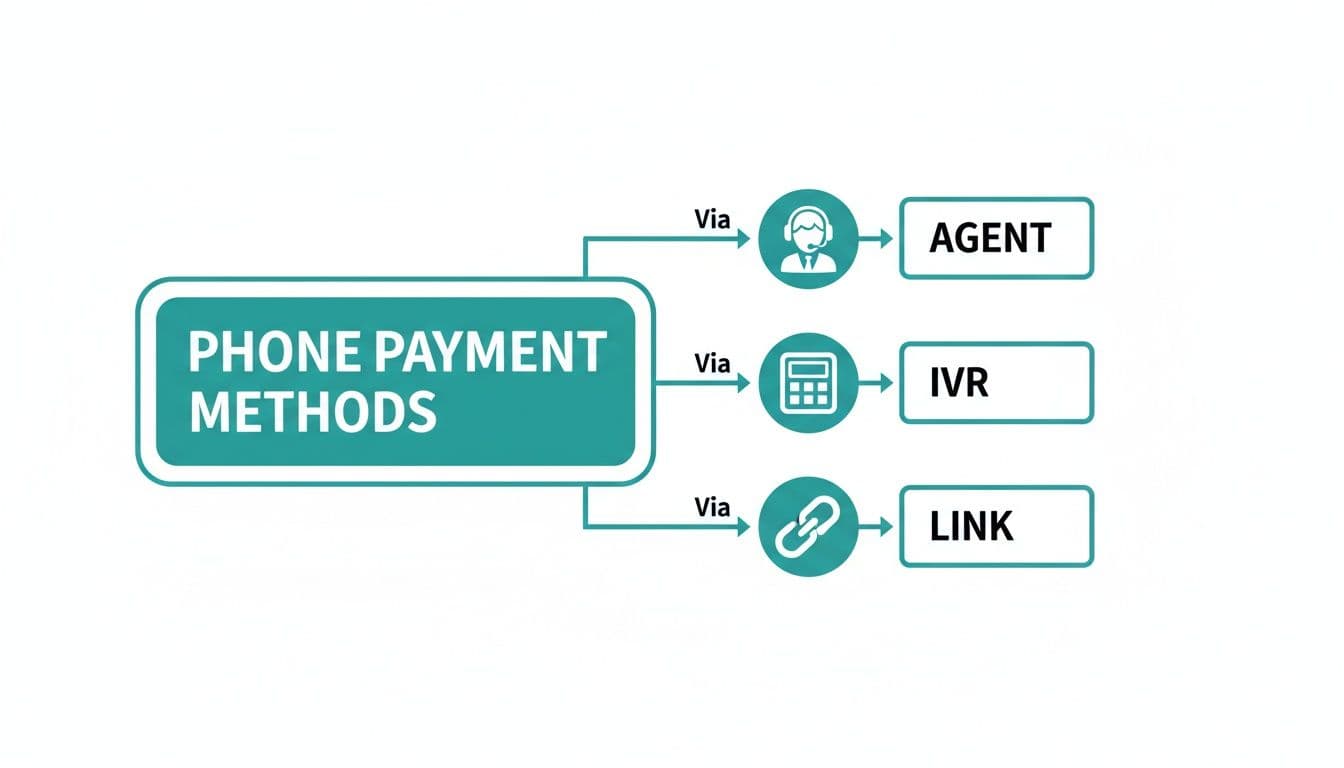

How to Take Card Payment Over the Phone Securely

Learn how to take card payment over the phone with our complete guide on PCI compliance, secure technologies, and best practices for your business.

Read article

A Guide to Secure Over The Phone Card Payments

Learn how to securely accept over the phone card payments. This guide covers the best methods, PCI compliance, and technology for UK businesses.

Read article

How to Take a Payment Over the Phone: A Secure Payments Guide

Learn how to take a payment over the phone securely with practical tips on PCI compliance, IVR, and masking to protect customers.

Read article

How to Securely Take Pay Over Phone Payments A Complete Guide

Learn how to take pay over phone payments securely. Our guide covers PCI compliance, essential tech, and best practices for contact centres and businesses.

Read article

A Complete Guide to Secure Card Payment Over Phone

Learn how to securely accept a card payment over phone. Our guide covers PCI compliance, modern technology, and best practices for contact centres.

Read article

A Guide to Accepting Card Payments Over the Phone Securely

Learn how to start accepting card payments over the phone securely. Our guide covers PCI compliance, best practices, and the latest payment technology.

Read article

Understanding the Credit Card Security Code

What is a credit card security code (CVV)? Learn where to find it, why it's your first defense against fraud, and how to handle it securely.

Read article

What is a debit card security code: Protect online payments and fraud

what is a debit card security code: find it on your card and learn why protecting it matters for online and phone payments.

Read article

Understanding what is security code on card and how it protects you

Learn what is security code on card, why it matters, and how this three-digit check helps protect your payments and identity.

Read articleHow AI Is Shaping the Future of Secure Payment Services

Discover how AI is revolutionizing secure payment services—enabling real-time fraud detection, data protection, and smarter digital transactions worldwide.

Read articlePayment Validation: Complete Guide | Paytia

Learn how payment validation works, why it's critical for secure transactions, and how to implement effective validation processes that protect your business and customers.

Read article![Is It Safe to Give Card Details Over the Phone? [2026 Guide]](/_next/image?url=%2Fimages%2Fblog%2Fblog-accepting-credit-card-payments-over-the-phone.webp&w=3840&q=75&dpl=dpl_7yXCNK2G5gRSuoR1P31G9ZBeTkRW)

Is It Safe to Give Card Details Over the Phone? [2026 Guide]

Learn how to safely share card details over the phone, recognize secure payment processes, identify red flags, and protect yourself from fraud when making phone payments.

Read article

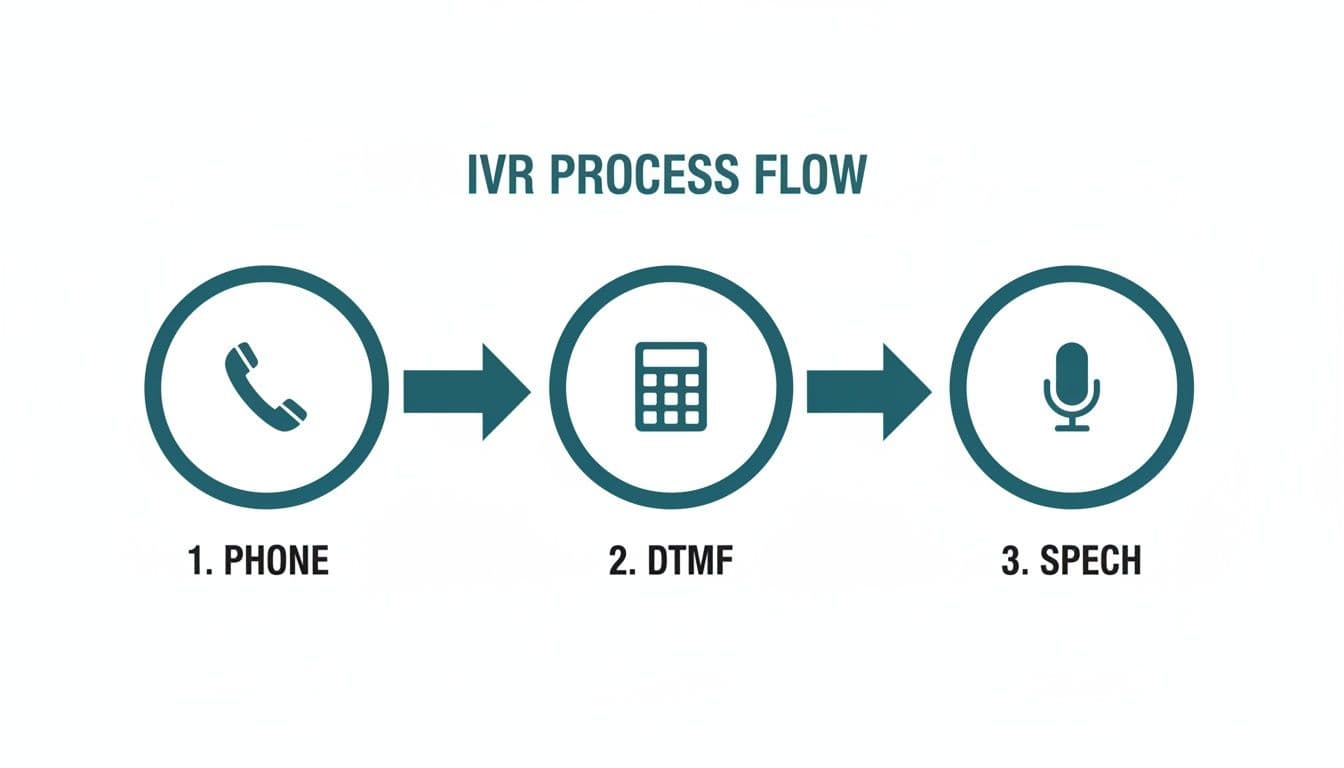

A Guide to Contact Center IVR for Seamless Customer Interactions

Discover how a modern contact center IVR can enhance customer experience, secure payments, and boost efficiency. Get expert strategies in our ultimate guide.

Read article

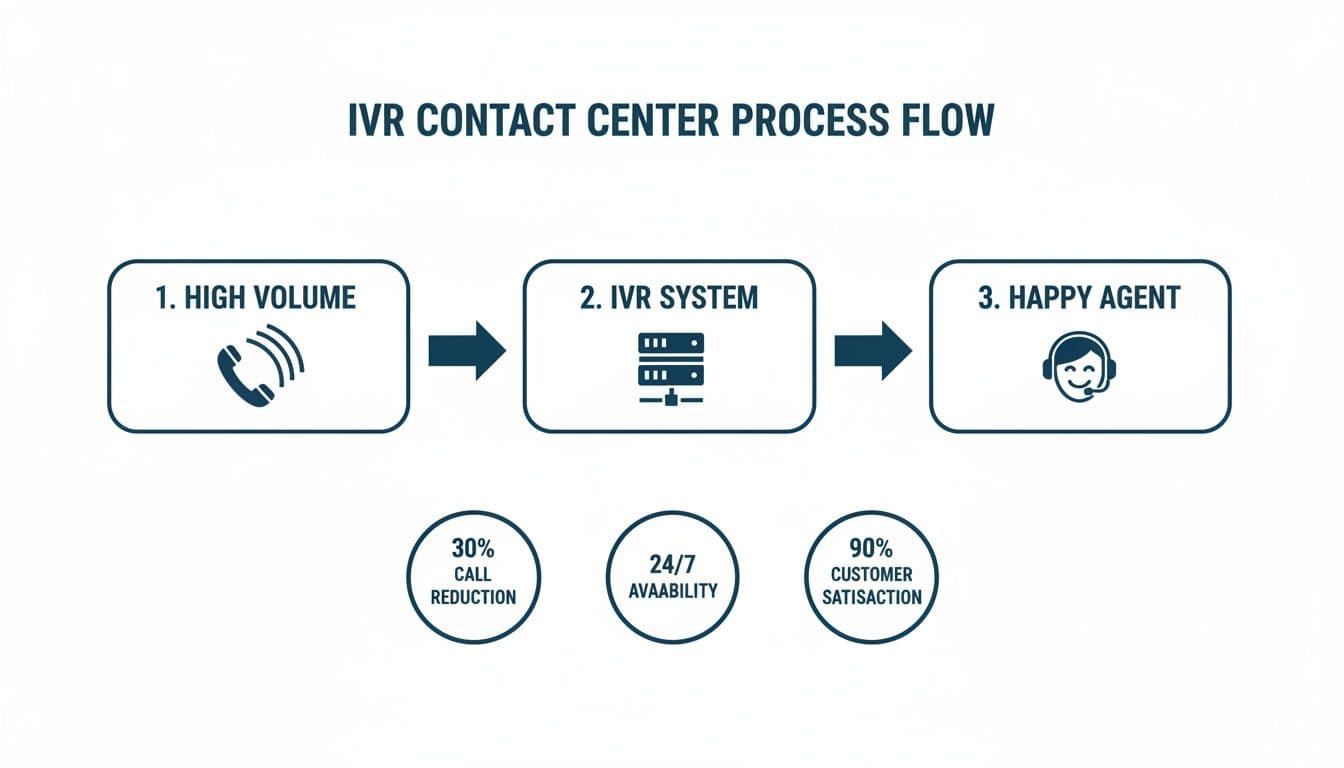

Your Essential Guide to the IVR Contact Center

Discover how an IVR contact center streamlines customer service, secures payments, and ensures compliance. A practical guide to implementation and optimization.

Read article

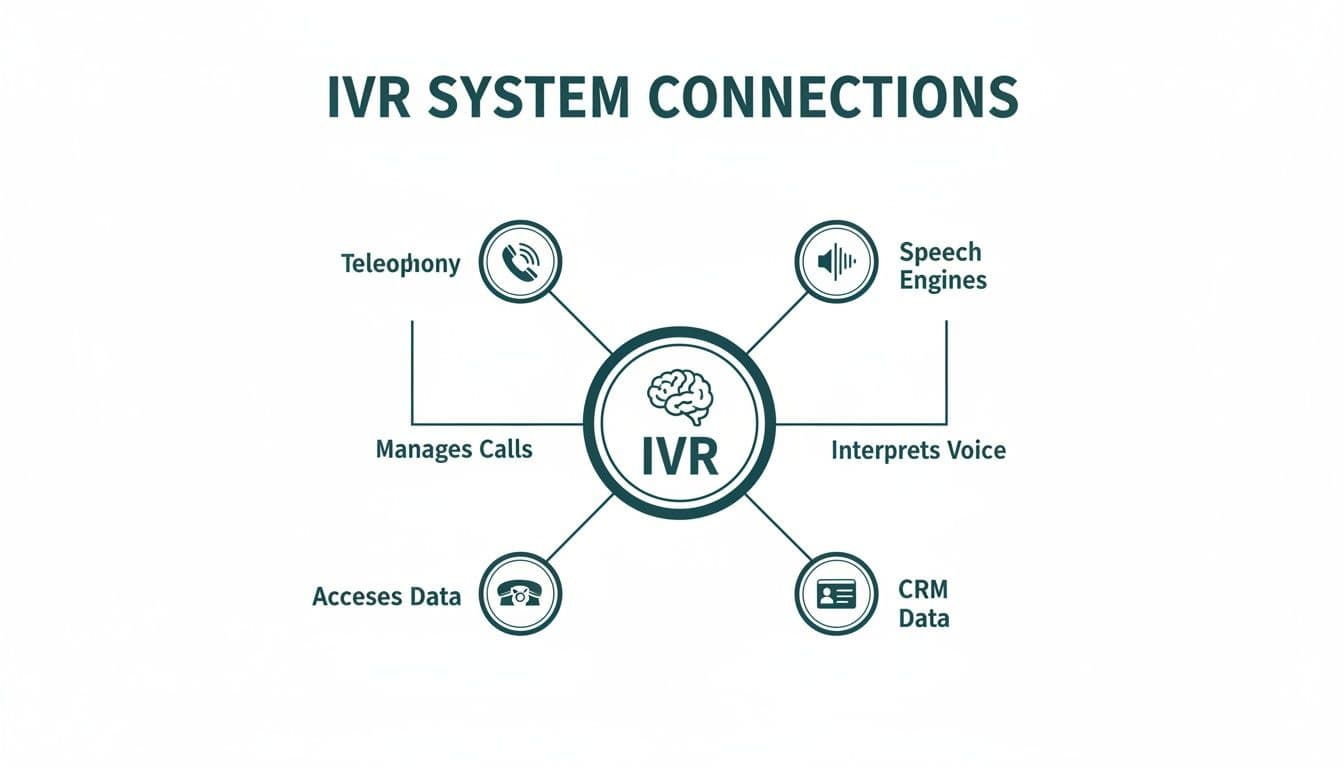

Your Complete Guide to the IVR Interactive Voice Response System

Discover how an IVR interactive voice response system transforms customer service and secures payments. Learn how it works and why it's vital for your business.

Read article

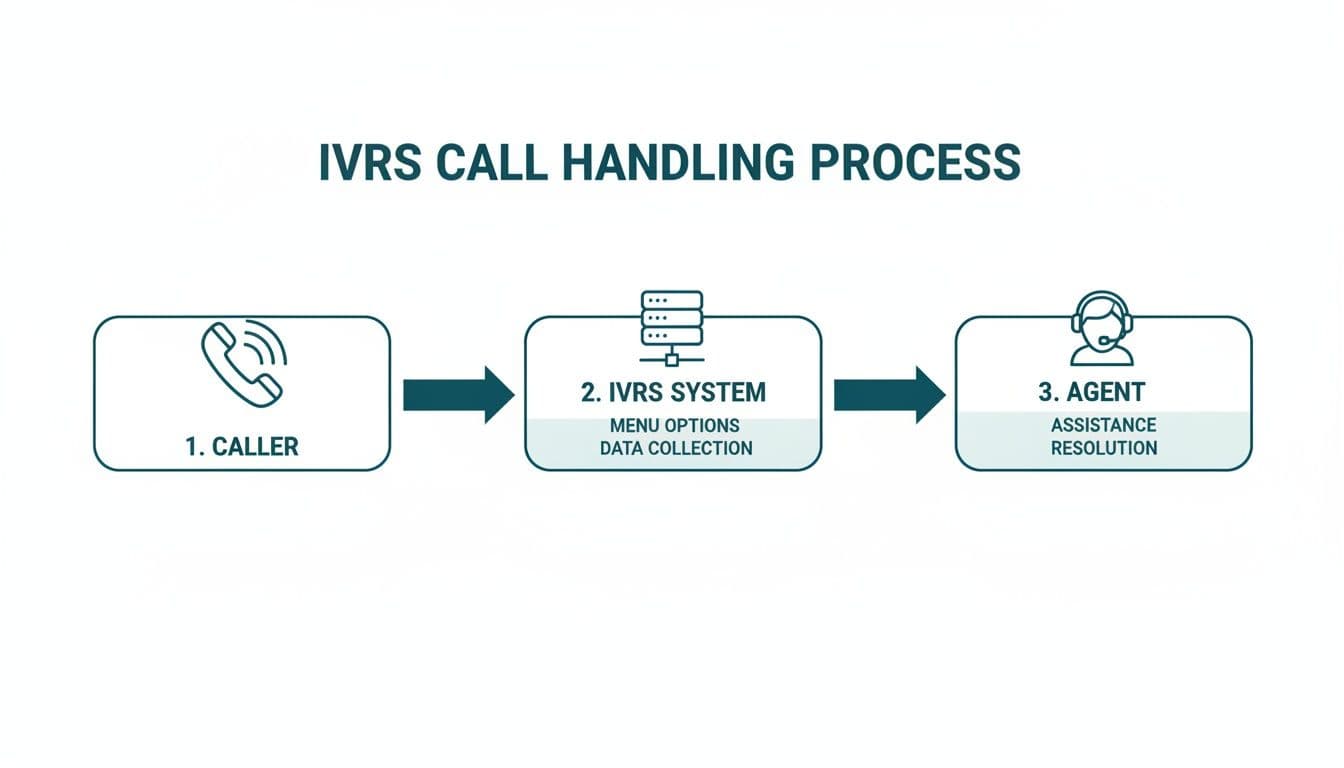

A Guide to Your Interactive Voice Response System IVRS

Explore the complete guide to an interactive voice response system IVRS. Learn how it works, its benefits, and how to implement secure IVR for your business.

Read article

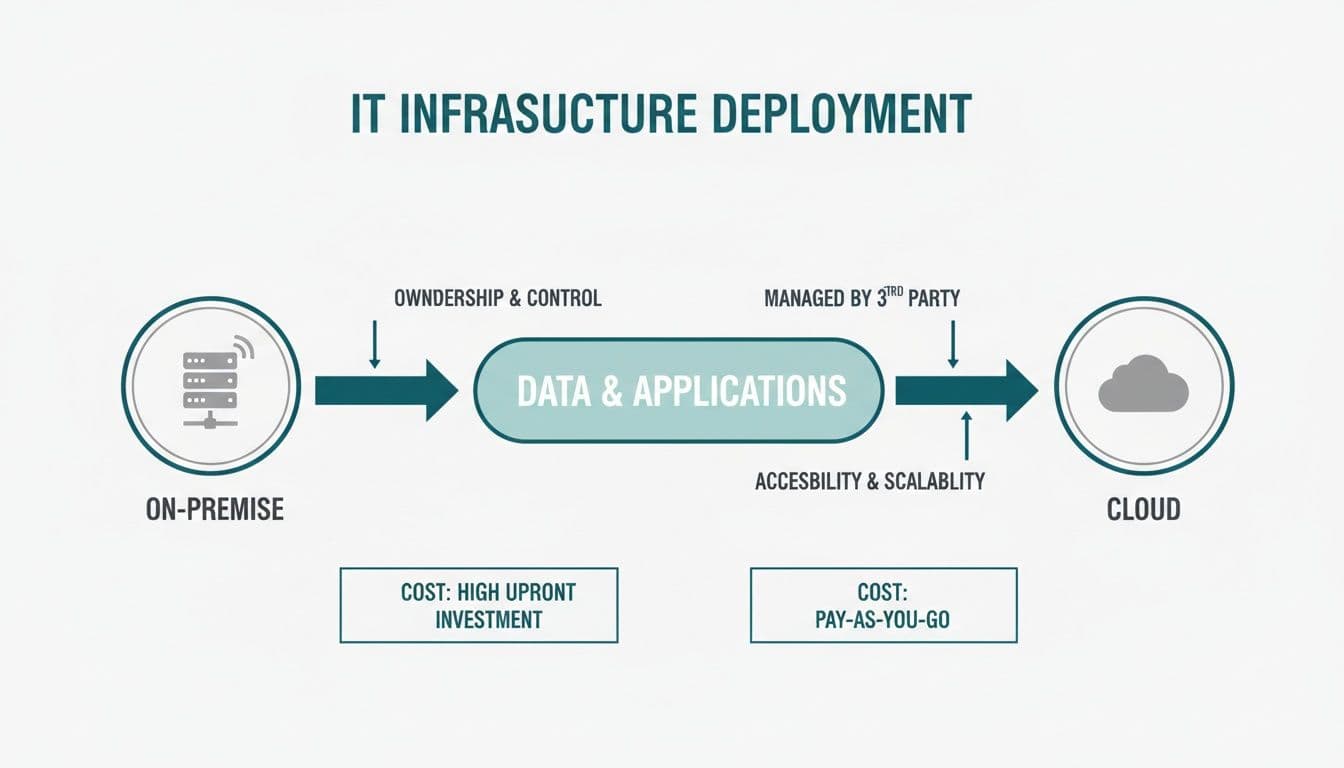

A Practical Guide to Cloud Contact Center Solutions

Discover how cloud contact center solutions transform customer service. Learn about key features, security, integration, and planning a successful migration.

Read article

A Practical Guide to IVR for Call Center Success

Discover how a modern IVR for call center transforms customer service. Learn to streamline routing, secure payments, and boost operational efficiency.

Read article

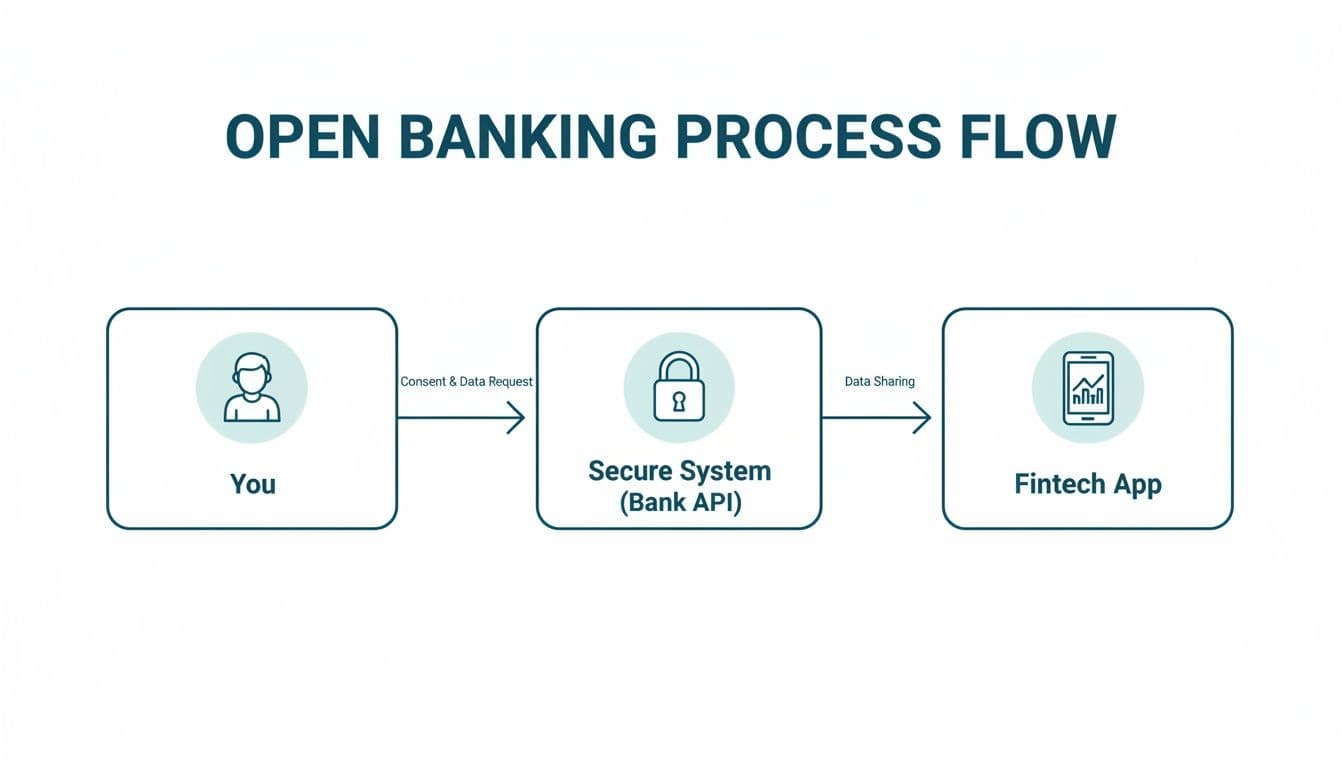

How Does Open Banking Work An Essential Guide

Discover how does open banking work with our clear guide. Learn about APIs, PSD2, and the real-world benefits for secure business payments.

Read article

What is click to pay: A Faster, Safer Online Checkout

Discover what is click to pay and how this secure, tokenized checkout streamlines online payments with a single, password-free click.

Read article

What Is a BT Payment Line and How Does It Work?

Discover what a BT payment line really is, the hidden risks of phone payments, and how modern solutions ensure your contact centre is secure and compliant.

Read article

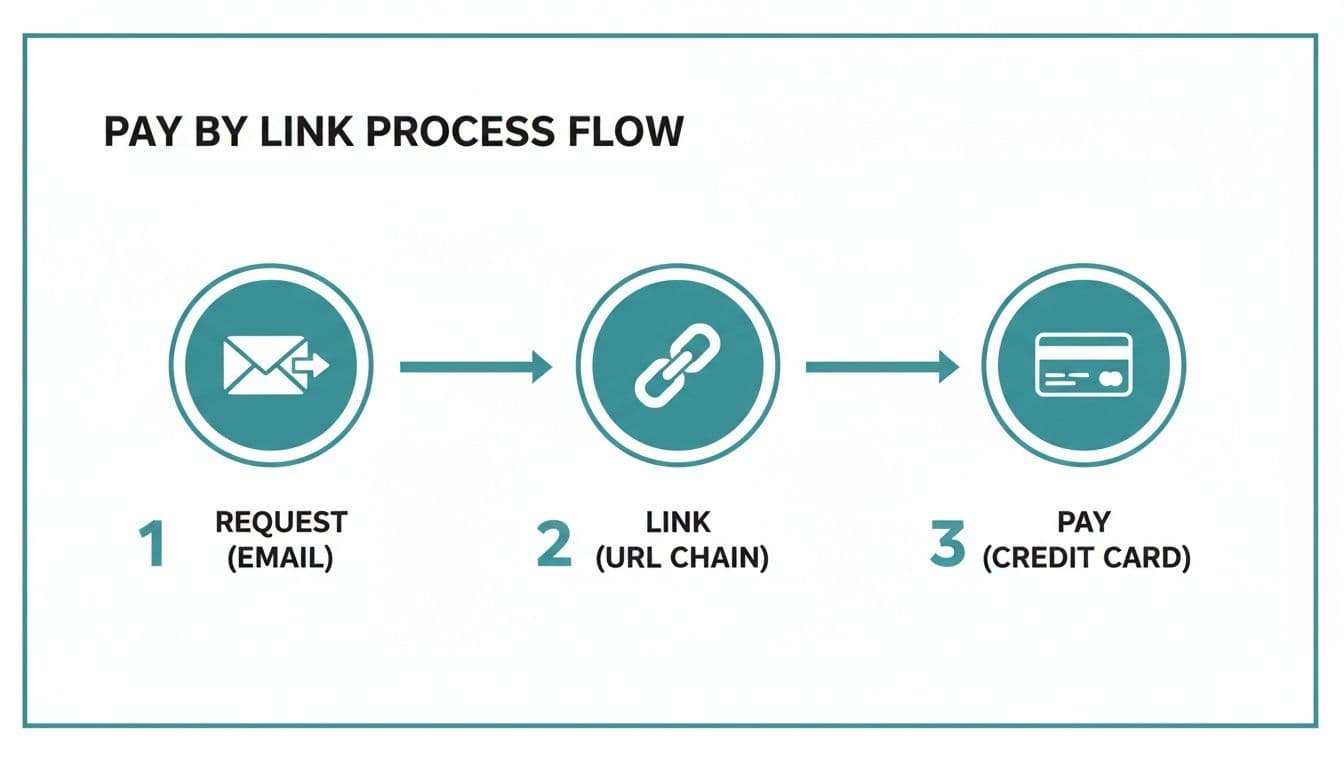

How Pay by Link Creates Secure and Seamless Payments

Discover how pay by link transforms transactions with enhanced security and convenience. Learn why it's a game-changer for businesses seeking secure payments.

Read article

What Is Tokenization And How It Secures Your Data

Curious about what is tokenization? This guide explains how it works, why it's different from encryption, and how it protects sensitive payment data.

Read article

A Guide to Merchant Credit Processing for Modern Businesses

Master merchant credit processing with our guide. Learn about fees, security, PCI compliance, and how to choose the right system for secure, efficient payments.

Read article

What Is a Customer Ref Number and Why Is It Key to Secure Payments

Unlock the power of the customer ref number. Learn what it is, where to find it, and how it’s essential for secure, efficient payment processing.

Read article

Balancing Security and Customer Trust in Phone Card Payments

Combine PCI controls with conversation-led service to keep customers paying confidently while you stay compliant.

Read article

Business Benefits of Secure Phone Payments and Compliance

Secure phone payments are not just a compliance cost—they free agents to close revenue, boost customer trust, and simplify audits.

Read articleSecure Phone Payment Solutions Built for Small Businesses

Small businesses can deliver enterprise-grade phone payment security with Paytia, reducing PCI scope and keeping customers confident.

Read articlePayment Security Builds Customer Trust (Revenue) | Paytia

How Payment Security Builds Customer Trust (And Why It Matters for Revenue) Your customers don't just want to pay you—they want to trust you. Payment se...

Read articleHow Business System Integration Drives Growth

Many organisations rely on multiple tools—CRM, accounting software, HR platforms, and customer support systems—but without proper integration, these tools create inefficiencies. Business system integration helps streamline operations, eliminate data silos, and improve decision-making.

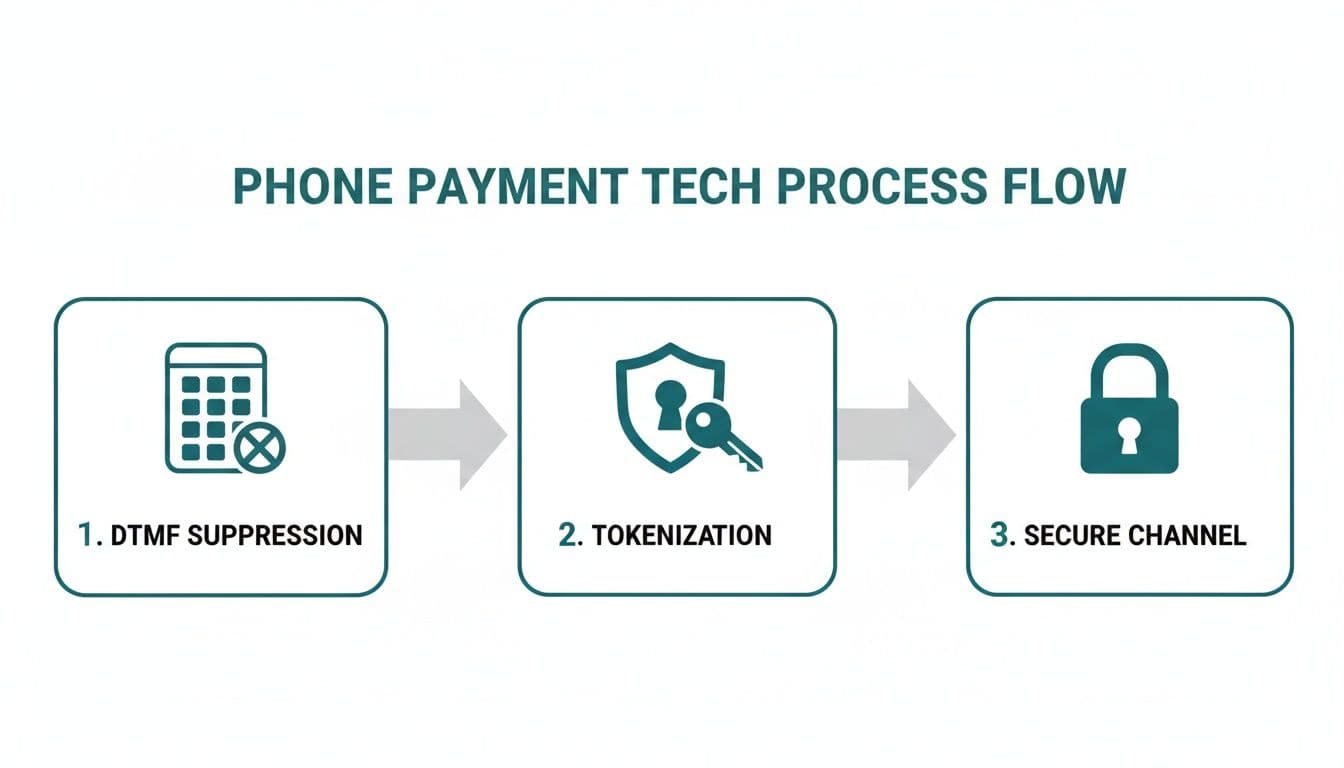

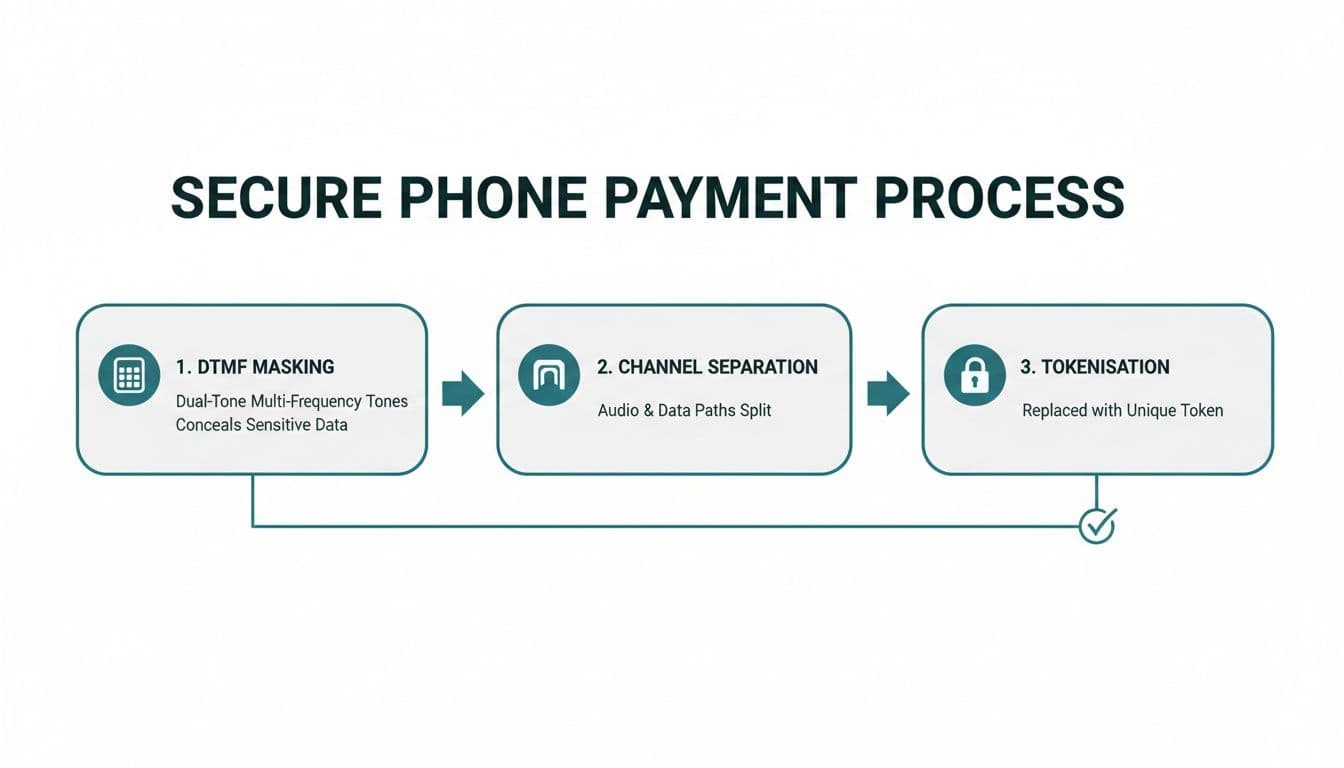

Read articleTaking Card Payments Over the Phone: UK Regulations & Security Guide (2026)

How to take card payments over the phone safely and legally in the UK. Covers PCI DSS compliance, DTMF masking, FCA consumer duty, and step-by-step guidance for secure telephone payments.

Read article

How to Comply With GDPR For Phone Payments

Phone payments must comply with GDPR regulations in addition to PCI DSS. Learn the specific requirements and how to implement compliant phone payment processes.

Read article

UK Regulations for Taking Card Payments by Phone

Phone payments in the UK are subject to multiple regulatory frameworks. Learn about PCI DSS, GDPR, FCA, and other requirements that affect how you process payments.

Read articleEnhancing Phone Payments with Aircall and Paytia

Combine Aircall’s flexible cloud telephony with Paytia’s secure payment capture to keep every call compliant.

Read article

Stripe + Paytia: Phone Payment Partnership | Paytia

Understand how Paytia complements Stripe by securing phone payments, simplifying PCI scope, and maintaining a unified reporting experience.

Read articlePaytia and Aircall: Phone Payment Partnership | Paytia

Paytia partners with Aircall to bring secure payment capture to cloud phone users. Agent Capture Assist technology enables PCI compliant telephone payments with DTMF masking.

Read articlePaytia and Talkdesk: Payment Partnership | Paytia

Discover how integrating Paytia secure payments with Talkdesk CX Cloud strengthens PCI compliance and keeps agents productive.

Read articleThe Complete Guide to PCI DSS Compliance for UK Businesses

Everything UK businesses need to know about PCI DSS compliance — levels, requirements, costs, scope reduction, and phone payment security.

Read articlePhone Payment Security: Everything You Need to Know

The complete guide to phone payment security — DTMF masking, PCI compliance, fraud prevention, and why pause and resume isn't enough.

Read articleHow Payment Processing Works: A Complete Guide

How card payments are processed from authorisation to settlement. Understand processors, gateways, interchange fees, and the complete transaction lifecycle.

Read articleDigital Payment Platforms: The Complete Guide for UK Businesses (2026)

Compare the best digital payment platforms for UK businesses in 2026. Learn how to choose the right platform for online, phone, and in-person payments, with pricing, security, and integration guidance.

Read article

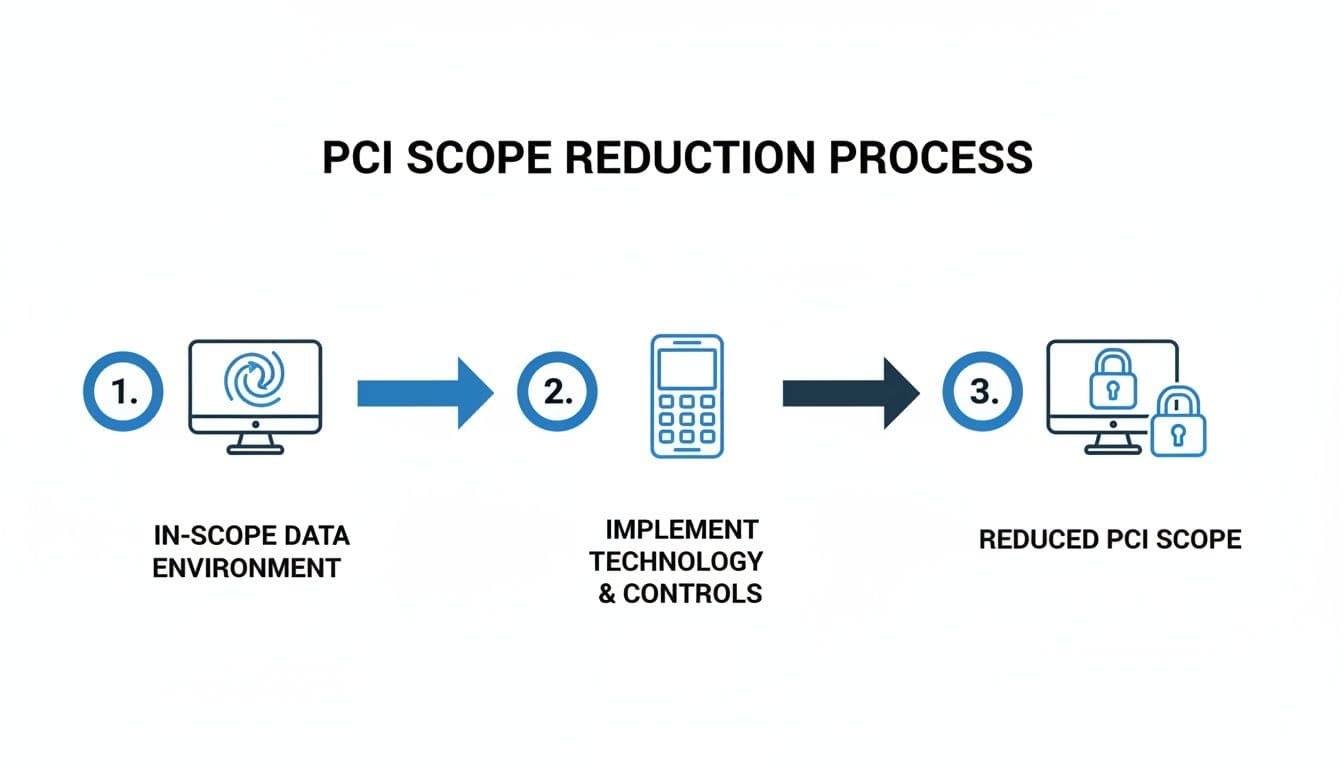

What Is Cardholder Data Environment a Guide to PCI DSS Scope

Understand what is cardholder data environment (CDE) with this practical guide. Learn how to define your PCI DSS scope, reduce risk, and cut compliance costs.

Read article

Sip: sip communication protocol Demystified for Modern Telephony

Discover how the sip communication protocol powers modern telephony, security, and PCI-compliant payments.

Read article