Merchant services fees are one of those areas where the headline rate in a sales pitch and the actual amount on your monthly statement often don't match. The structure of card payment fees has several layers, and providers have different ways of bundling and presenting them. Once you understand how the fee structure works, you can make a much more informed comparison between providers — and spot the charges that only appear in the contract small print.

The Three Layers of a Card Payment Fee

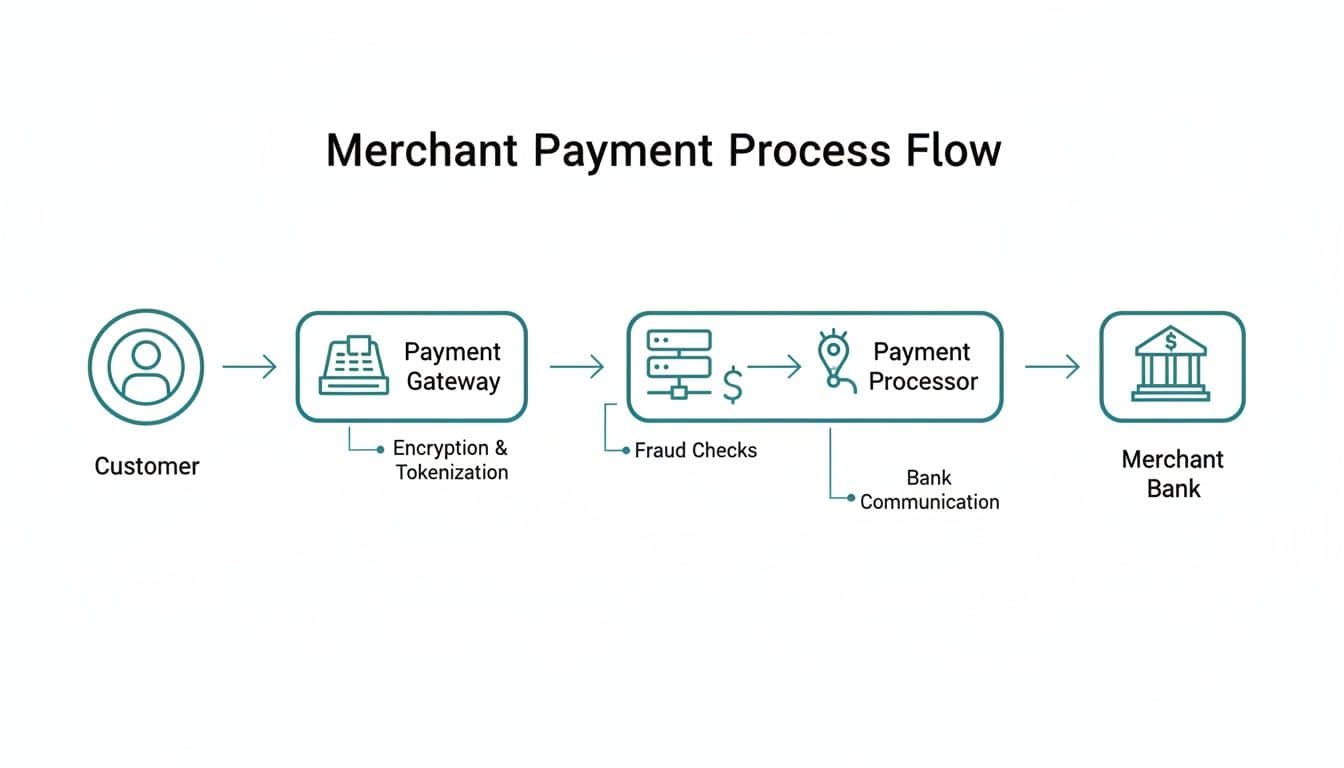

Every card transaction you process involves three entities taking a slice: the card issuer (your customer's bank), the card scheme (Visa, Mastercard, Amex), and your acquirer (the organisation that processes payments on your behalf). The fee you pay to your acquirer is supposed to cover all three, but it's worth understanding what's in each layer.

Interchange

Interchange is the fee paid to the issuing bank — the bank that gave your customer their card. When your customer pays you with a Barclays Visa debit card, Barclays gets an interchange fee from that transaction.

Interchange rates are set by Visa and Mastercard, not by your acquirer. They vary by card type, card region, and transaction method. Under EU and UK regulations following Brexit, interchange on consumer debit cards is capped at 0.2% and on consumer credit cards at 0.3%. Business cards (corporate cards, company expense cards) are not subject to these caps and can have interchange rates of 1.5% to 2.5% or more.

This is why your effective rate is often higher than you expect when a significant portion of your customers pay with corporate cards — the interchange component alone can be much higher than the consumer card cap.

Scheme Fees

On top of interchange, Visa and Mastercard charge scheme fees for accessing their network — the infrastructure that handles the authorisation and settlement process. These are typically a small percentage (0.1% to 0.3%) plus sometimes a per-transaction amount.

Scheme fees have been increasing steadily. Visa and Mastercard periodically adjust these, and some acquirers pass through increases automatically, while others absorb them. If your contract says "scheme fees may change," that's worth paying attention to.

Acquirer Markup

The acquirer — Worldpay, Barclaycard, Stripe, Adyen, Paytia, or whoever processes your payments — adds their own margin on top of interchange and scheme fees. This is where the actual negotiation happens, because interchange and scheme fees are fixed; the acquirer markup is the commercial part.

Acquirer markups range from very thin (0.1% to 0.2% for high-volume merchants negotiating directly) to several percentage points for small businesses on "blended" pricing where the provider bakes all the layers into a single rate and presents it as a simple number.

How Pricing Models Differ

The way these layers are presented to you depends on the pricing model your provider uses.

Blended Pricing

The most common for small businesses. You're quoted a single rate — say, 1.75% — that covers interchange, scheme fees, and the acquirer margin. It's simple to understand, but you're paying the same rate regardless of whether your customer uses a cheap debit card (where the interchange cost to the provider is low) or an expensive corporate card (where it's high). On high-volume or high-average-transaction businesses, blended pricing often costs more than it should.

Interchange Plus (IC+) Pricing

You're charged the actual interchange rate for each transaction, plus a fixed acquirer margin. If a transaction has interchange of 0.2% and your acquirer margin is 0.5%, you pay 0.7% for that transaction. If a corporate card with 1.5% interchange processes a transaction, you pay 2.0%.

IC+ pricing is more transparent and is typically cheaper for businesses with a predictable card mix dominated by domestic consumer debit cards. It's more unpredictable when your customer base uses a wide variety of card types.

Flat-Rate Pricing

Popularised by Square and Stripe. A single rate applies to all transactions — typically around 1.4% to 2.9% depending on the transaction type. Simple, predictable, no monthly fees in some cases. Works well for very small businesses or those with low and variable volumes, where the simplicity is worth paying slightly more per transaction.

Gateway Fees

Separate from the transaction rate, many providers charge a gateway fee — the cost of accessing the payment infrastructure that connects you to the card schemes. This is sometimes included in the transaction rate, but often appears as a separate line:

- Monthly gateway subscription: £15 to £50 per month is typical

- Per-transaction gateway fee: 5p to 20p per transaction, applied on top of the percentage rate

If you're processing 1,000 transactions a month with a 10p per-transaction gateway fee, that's an extra £100 per month that won't appear in a headline rate comparison.

Hidden Fees to Watch For

These are the charges that tend to appear on statements without being prominently disclosed in initial conversations.

PCI Non-Compliance Surcharge

If you haven't completed your annual PCI DSS self-assessment questionnaire (SAQ) or evidenced compliance, many acquirers charge a non-compliance surcharge — typically £20 to £50 per month. This continues until you remediate and provide evidence of compliance. For businesses that ignore PCI requirements, this can run for years without anyone noticing it on the statement.

Monthly Minimum

Some contracts include a monthly minimum transaction volume or value. If your business is seasonal or you're just starting out, you may be charged a fee to make up the difference between what you actually processed and the minimum in the contract. Always check whether there's a monthly minimum and what the cost is if you fall below it.

Authorisation Fees

Some providers charge for each authorisation request — including failed ones. A customer whose card declines still costs you the authorisation fee. This is usually a few pence per transaction but adds up if you have a high decline rate.

Chargeback Fees

When a customer disputes a transaction and initiates a chargeback through their bank, the acquirer typically charges you an admin fee — £15 to £25 per chargeback is common — regardless of whether you win or lose the dispute. High-volume businesses or those in sectors with elevated dispute rates need to factor this in.

Early Termination Fees

Many merchant services contracts have a minimum term (12 to 36 months is common) and charge an early termination fee if you cancel before the end of the term. These can be substantial — sometimes the equivalent of several months of the monthly minimum fee. Always check the exit clause before signing.

How Paytia's Pay-Per-Transaction Model Compares

Paytia charges per transaction with no monthly subscription, no setup fee, and no contract minimum term. You pay when you process a payment, and nothing when you don't.

This is particularly relevant for businesses where payment volumes vary — seasonal businesses, businesses still scaling up, or businesses where telephone orders are a secondary rather than primary sales channel. A fixed monthly fee or monthly minimum doesn't suit those profiles; a per-transaction model does.

The absence of a long-term contract also means you're not locked in. If your needs change, or if a different provider makes more sense for your volume or card mix at a later stage, you're not paying an exit penalty to switch.

Pay by Bank: The 0.5% Alternative

For higher-value transactions, Pay by Bank (open banking payments) is worth serious consideration. Rather than routing through the card scheme, Pay by Bank initiates a direct Faster Payments transfer from the customer's bank to yours. It settles within seconds and typically costs around 0.5% — substantially less than card transactions, particularly for credit card payments.

The trade-offs: customers need to approve the payment through their own bank's app, which takes slightly longer than a tap or card entry. Some customers find this process unfamiliar. And there's no chargeback mechanism — once the money is transferred, it's there (which is good for merchants, though it means fraud protection relies more on the bank's authorisation controls).

For businesses regularly processing transactions over £500, the fee difference between 2.5% card and 0.5% Pay by Bank is significant enough to be worth offering both options and letting customers choose.

Paytia supports Pay by Bank alongside card payments within the same payment link — so you can present both options in a single payment request and let the customer decide which they prefer.

Making Sense of Your Current Fees

If you're trying to understand what you're currently paying, the most useful exercise is to take your last three monthly statements and calculate your effective rate: total fees divided by total card volume processed. Compare that to the headline rate you were quoted when you signed up.

If there's a significant gap — and there often is — it's worth going back to your provider and asking them to itemise the charges. You may find that the PCI non-compliance surcharge has been running for months, or that a higher-than-expected volume of corporate card payments is inflating your average rate.

If you want to compare what Paytia's pricing would look like for your current volumes and transaction types, get in touch and we can give you a specific comparison.