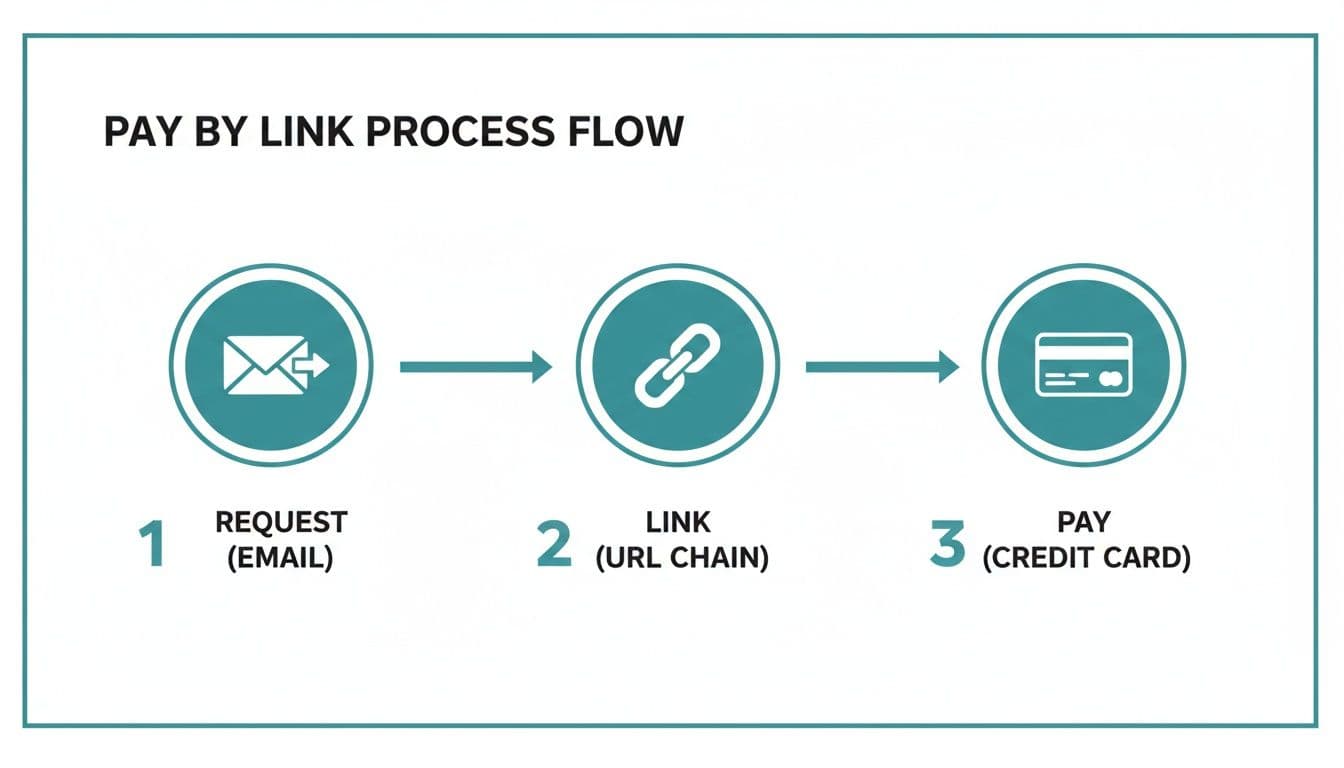

SMS payment links — sometimes called pay by text — are one of the most practical additions to the UK business payment toolkit in recent years. The concept is simple: send a text message with a link, the customer taps it, and they're taken to a hosted checkout where they complete the payment. No app required, no login, no account creation.

The numbers make the case for why this works: SMS has an open rate of around 98%, compared to roughly 20% for email. The average customer completes a payment via SMS link in approximately 30 seconds from clicking the link to receiving a confirmation. For businesses chasing outstanding invoices or collecting payment for completed services, those figures are hard to ignore.

How SMS Payment Links Work

At the technical level, a pay by SMS transaction works like this:

- Your business (or your payment platform) sends a text message to the customer's mobile number. The message typically includes a short description of what the payment is for, the amount, and a link.

- The customer taps the link on their phone. They're taken to a hosted checkout page — a secure webpage run by the payment processor, not stored on your servers.

- The customer enters their card details (or uses Apple Pay / Google Pay if their device supports it), confirms the amount, and submits.

- The payment is processed through the card scheme in the usual way. The customer receives a confirmation, and your business receives notification of the successful payment.

The key point from a security and compliance perspective is that no card data ever travels through the SMS. The link in the text takes the customer to a PCI-compliant checkout environment. The SMS itself is just a delivery mechanism for the link — it contains no payment data.

Use Cases Where Pay by SMS Works Well

Overdue Invoice Collection

For businesses with outstanding invoices, SMS payment links are considerably more effective than emailed invoice reminders. Email reminders get ignored. They sit in inboxes, get buried by other messages, and require the customer to actively go looking for the invoice. An SMS arrives on the device the customer checks most frequently, and the link is right there to tap.

Paytia's Payment Chase feature automates this process. When an invoice goes unpaid past its due date, Payment Chase can send a series of SMS messages at defined intervals — each with a unique payment link for that specific invoice. The sequence continues until the payment is made, at which point it stops automatically. The business doesn't need to manage the follow-up manually.

Appointment and Service Reminders

Businesses that take bookings — dental practices, hair salons, consultants, repair services — can include a payment link in appointment confirmation or reminder texts. Customers who want to pay ahead of their appointment can do so in seconds. For no-show-prone bookings, this can also function as a soft deposit mechanism.

Post-Service Payment for Field Operatives

Plumbers, electricians, IT support engineers, and other field-based workers often complete jobs and then have an awkward conversation about payment. The customer doesn't have a card machine to hand. The operative doesn't carry one. A payment link sent by SMS while the operative is still on site solves this — the customer taps the link, pays immediately, and both parties have confirmation before the operative leaves.

Donation Collection for Charities

Charities with existing donor relationships can use SMS payment links for campaign-specific donation asks. The conversion rate from an SMS link is typically higher than from a mail appeal or email link, particularly for existing supporters who've donated before and just need a prompt and a payment mechanism.

Contact Centre Follow-Up

In a contact centre context, an agent who can't complete a payment during a call — perhaps the customer doesn't have their card to hand, or they want to check something before authorising the charge — can send a payment link to the customer's mobile at the end of the call. The customer completes it when it's convenient for them, and the agent doesn't need to call back.

UK Compliance Requirements for SMS Payments

PCI DSS

As noted above, no card data travels through SMS — the link simply takes the customer to a hosted checkout. This means SMS is not itself within PCI scope. The hosted checkout is within PCI scope, which is why you need to ensure you're using a PCI-compliant payment provider for the checkout page. Using Stripe, PayPoint, or a specialist provider like Paytia handles this — you don't need to build or host the checkout yourself.

PECR (Privacy and Electronic Communications Regulations)

PECR governs marketing messages sent by SMS in the UK. The key rule is that you can't send unsolicited marketing by SMS without prior consent. For payment messages — where you're contacting an existing customer about a transaction they have an outstanding obligation for — these are generally considered transactional or service messages rather than marketing, and prior consent requirements are less stringent.

However, the line between a payment reminder and a marketing message can blur. An SMS that says "You have an outstanding invoice — click to pay" is clearly transactional. An SMS that says "Don't miss out — settle your account and get 10% off your next order" has crossed into marketing territory and requires explicit prior consent.

For UK businesses, the practical guidance is: keep payment SMS messages factual and specific to the transaction. Don't include promotional offers or upsells. Include an opt-out mechanism if you're sending repeated messages. Check the ICO's PECR guidance if you're unsure about a specific use case.

ICO Registration

Any UK business that processes personal data — which includes customer phone numbers used to send payment texts — needs to be registered with the ICO (Information Commissioner's Office) under UK GDPR. Registration costs £40 to £60 per year for most small businesses and is separate from PCI compliance. If you're not already registered, check whether you need to be at ico.org.uk.

What to Look for in a Pay by SMS Provider

When evaluating SMS payment solutions for your business, these are the key factors:

- PCI compliance of the hosted checkout — The link must take customers to a checkout that meets PCI DSS standards. Ask for the provider's PCI certification details.

- Apple Pay and Google Pay support — Many customers will complete payment faster using stored cards on their device rather than typing card details manually. Checkout pages that support digital wallets typically have higher completion rates.

- Branded checkout pages — A checkout page that looks like it's from an unknown company creates hesitation. Customised checkout pages with your business name and branding improve customer confidence.

- Tracking and reporting — Can you see whether a link was delivered, opened, and completed? This data is useful for understanding where drop-offs occur and for prioritising follow-up.

- Automated sequences — For invoice collection, can the system send follow-up messages automatically rather than requiring manual intervention for each unpaid invoice?

- Integration with your existing systems — Does it connect with your accounting software, CRM, or customer database so that payment confirmations update your records automatically?

SMS vs Email for Payment Collection: A Comparison

The case for SMS over email for payment requests comes down to attention. Email inboxes are full. SMS inboxes, particularly for transactional messages from businesses, are considerably less crowded.

That said, email has its place — particularly for sending formal invoices with itemised breakdowns, or for customers who prefer to have a written record in their inbox. The most effective approach for many businesses is both: send the invoice by email for the formal record, and send an SMS with the payment link for the actual payment prompt.

Paytia's payment link and Payment Chase features support both channels, and the reporting shows you which channel is getting better results for your specific customer base — so you can make an evidence-based decision about where to focus.

If you want to see how SMS payment links would work for your business's payment collection process, get in touch.