DTMF Masking Secure Payments With the Human Touch

Your Agent Stays, Card Data Doesn't

The call keeps going. Card data doesn't reach you.

How DTMF masking works

Customer

Enters card details via phone keypad

Real DTMF tones generated

Real tones

Paytia Platform

Captures real tones and processes payment securely

Card data stays here — never reaches you

Masked tones

Agent

Hears flat replacement tones, stays connected

Zero access to card data

Customer

Enters card details via phone keypad

Paytia Platform

Captures real tones, masks them, processes payment securely

Agent

Hears flat replacement tones, stays connected throughout

How DTMF masking actually works on a live call

Every keypress on a phone produces a pair of audio frequencies — one low, one high. That's where the “dual-tone multi-frequency” name comes from. Press “5” and the handset emits 770 Hz alongside 1336 Hz. The low group runs 697, 770, 852 and 941 Hz; the high group runs 1209, 1336, 1477 and 1633 Hz.

Every key on the pad maps to a unique pair. The two-tone design exists because a single tone could be imitated by a human voice or background noise — a precise simultaneous pair can't be. Telephone networks have been decoding those tones into digits since Bell Labs invented the standard in the 1960s.

That's why a card number can travel over a phone call at all. It's also why the agent can hear it, why the call recorder captures it, and why a sticky note left by the desk three hours later is still a card data leak waiting to be auditioned.

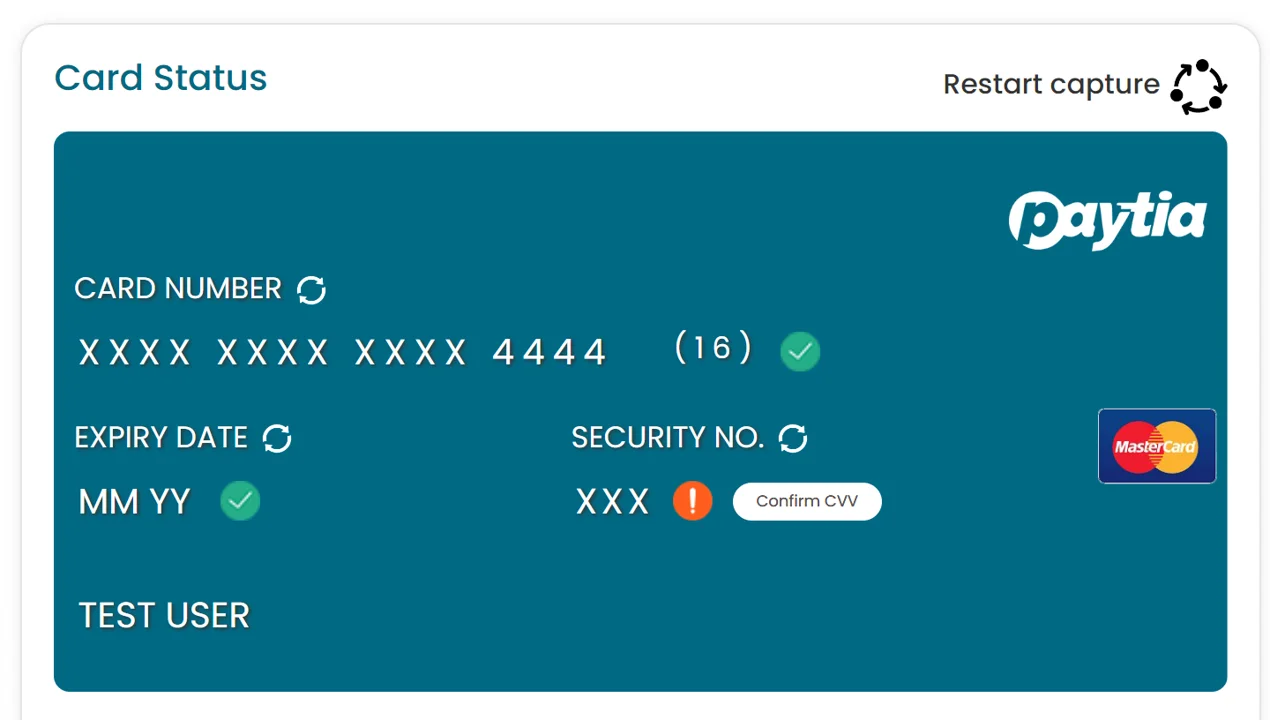

We sit in the audio path between the customer and your agent. When the agent decides it's time to take payment, they enter the amount in our agent terminal and press one key — usually 729 — to start the capture. The customer hears a short voice prompt asking them to enter their card on their handset.

From that moment, every DTMF tone the customer generates gets caught by our platform, decoded into the actual digit, and sent over an encrypted channel directly to your payment processor. The agent's leg of the call gets a flat replacement tone instead of the real one — a soft, identical-sounding chirp that tells them “something was pressed” but reveals nothing about which digit. The recording layer captures that same flat tone. So does any QA platform that's pulling audio from the trunk.

The voice channel stays open the whole time. If the customer asks “is this the right card?” or “what was the total again?” the agent answers normally — they just can't hear the digits being entered. The agent screen shows a masked indicator — **** **** **** 1234 once the full card number, expiration and CVV are in — so they can see the capture is progressing without seeing the numbers themselves.

When the processor returns an authorization, the agent sees the result on screen (paid, declined, or retry) and picks the conversation back up: “That's gone through, thanks — I'll email your receipt now.” The whole capture takes 20 to 30 seconds for most cards. There's no transfer to an IVR, no “please hold while I connect you to our payment system” — the call doesn't go anywhere.

The technical detail that matters here is wherethe interception happens. A naive implementation that detects tones and then replaces them can let a fraction of the first tone — a “bleed” — escape into the agent path before the replacement kicks in. The PCI Security Standards Council's telephone payments guidance flags DTMF bleed specifically. Our implementation clamps the audio stream at both ends so no tone can leak under any timing condition. That's the difference between a control that passes audit day and one that holds up when a QSA actually starts pulling spectrograms.

A couple of details people ask about. The card number never sits in our systems beyond the few hundred milliseconds it takes to forward it to your processor — we're a transmission point, not a vault. If you want to take repeat payments from the same customer later, the processor tokenizes the card and gives you a token to keep; the original card number still never lives in your environment.

And because we're intercepting at the audio layer rather than relying on agent behavior, there's no “the agent forgot to start it” failure mode. If the agent skipped the capture and asked the customer to read the digits out loud the old way, you'd hear that on your recording — but the moment they press 729, masking is on, and there's nothing for the agent to remember to do correctly.

What this does to your PCI DSS scope

PCI DSS scope is determined by where cardholder data flows. Anywhere card data is stored, processed, or transmitted is in scope, and every system in scope has to meet the standard's controls.

Without DTMF masking, a typical contact center payment puts a lot of systems in the data path: the agent's headset and workstation, the agent's desktop applications, the call recording server, the QA platform that ingests recordings, the WFO tools that touch them, the network segments connecting all of that, the firewalls in front, and the directory services authenticating the agents.

That's the SAQ D scenario — 329 controls covering everything from network segmentation to vulnerability scans to formal incident response plans, audited annually. For most US contact centers that translates to $20,000 to $65,000 a year in audit costs alone, before you count the staff time.

With masking on, card data never reaches any of those systems. The customer's handset talks to our PCI DSS Level 1 platform, and we talk to your processor. That's the cardholder data environment, and you're not in it.

The recording stops being in scope because there are no card digits in the audio. The agent workstation stops being in scope because no card data reaches it. Your CRM stops being in scope because the agent never has digits to paste. Most of your network drops out for the same reason.

You move to SAQ A, which is 22 controls — most of them about picking a certified service provider, validating their attestation, and keeping your own organizational policies in order. It's the same SAQ used by businesses that take payment only via a hosted iFrame on their website.

The PCI Security Standards Council's information supplement Protecting Telephone-Based Payment Card Datarecognizes DTMF masking as a method that takes the telephony environment, the agent environment, and the CRM out of scope. That's the entire commercial logic of the control.

There's a quieter version of the same risk that organizations underweight: the rogue agent. Most contact center fraud doesn't come from external attackers — it comes from someone on the inside who can hear or see card digits and chooses to write them down. Once the data is in the agent's environment, no audit log will tell you a number went into a notebook.

The only reliable defense is making sure the data never reaches the agent in the first place, which is exactly what masking does. You're not asking your staff to behave well around card data — you're making it impossible for them to misbehave because the data isn't there.

A few things stay in scope and it's worth being honest about which. You're still responsible for the systems that handle the resultof the payment — order numbers, refund records, the customer record where you log “paid $49.99 on March 12.” That's not card data, but if you store the auth code, last four digits, or anything else returned from the processor, those records still need basic protection.

You're also still responsible for vetting Paytia: pulling our Attestation of Compliance every year, checking we're still on the PCI Council's registered service provider list, and including the validation in your own SAQ A submission. That's real work but it's an afternoon, not a quarter.

The numbers people care about: most of our customers report PCI compliance costs falling 80–90% in the first year, the audit itself going from a multi-week QSA engagement to a self-assessment, and recording retention becoming a non-issue. There's also a category of cost that's harder to quantify — the agent training, the “don't write that down” posters, the periodic spot-checks of the contact center floor — that simply stops being needed. If there's no card data for an agent to mishandle, you don't need a program to stop them mishandling it.

What changed under PCI DSS 4.0.1

PCI DSS 4.0.1 has been mandatory since March 31, 2025. Two of the changes hit telephone payments directly. The first is the treatment of call recording: any recording that captures sensitive authentication data after authorization completes is now an explicit control failure.

Pause-and-resume was already a weak control under earlier versions — under 4.0.1, an environment that depends on it has very little rope when an auditor finds the inevitable handful of recordings where the pause didn't fire. The reliable answer is to ensure the data isn't in the audio at all, which is what DTMF masking does at an architectural level rather than a behavioral one.

The second is segmentation. 4.0.1 expects clearer documented separation between in-scope and out-of-scope systems, and a properly descoped contact center is structurally easier to defend in this respect — card data never crosses the boundary, so the boundary is straightforward to evidence. For US contact centers, this also tracks cleanly alongside HIPAA obligations on healthcare payments (PHI stays out of the recording too, by the same architecture) and TCPA obligations around recorded calls — your recording stays continuous and complete, with the digits simply absent from the audio.

Why customers actually feel the difference

The compliance argument is the one that wins budget. The customer experience argument is the one that turns a payment line from a friction point into a revenue channel. Both matter, and one of them is harder to measure than the other.

Customers know when an agent can hear them entering card details. They feel it. We've had customers tell us they used to step outside, close their office door, or wait until they got home before making a payment call — because reading their card out loud or hearing the tones echo across the line in a quiet office felt like undressing in public.

Some would avoid the phone payment entirely and ask for an invoice, adding days or weeks to the cycle while you chased a payment that should have closed on the call. That friction translates directly into lost or delayed revenue, and it's invisible if you only look at conversion at the call level — the customer didn't abandon, they just asked to pay later, and a third of them never come back to it.

Open-plan offices are where this bites hardest. A finance manager paying a supplier from a shared workspace doesn't want everyone within three desks to hear the keypad tones — even if the actual digits can't be reconstructed by ear, the discomfort is enough to make them stop the call and pay another way.

Public spaces present the same problem, sharper. A customer on a subway platform, in an ER waiting room, or sitting in a coffee shop doesn't have the option of finding a private room. With masking on, they enter their card silently while the agent stays on the line to confirm the amount and answer questions — and the awkwardness simply isn't in the call any more.

Healthcare is an especially sharp case. A patient calling to pay a copay or settle an outstanding balance might be sitting in a ward, a family room, or a hospital reception. The payment itself is sensitive enough, but the context makes it worse — other patients nearby, family members in the room, staff walking past.

Masking means the payment happens quietly and privately while the billing agent stays on the line to confirm the amount and provide a reference. The same architecture keeps PHI out of the recording for HIPAA purposes, which is the other half of why hospital billing teams adopt it quickly.

Remote and hybrid working sharpened the same edge from the agent's side. A significant share of US contact center agents take payments from spare bedrooms and kitchen tables since 2020, with partners, kids and roommates in earshot.

Without masking, you're trusting every one of those agents to maintain physical security in a home they don't control. With masking, card data never reaches the agent's location regardless of where they happen to be sitting — the privacy protection is consistent across head office desks, home offices and co-working spaces.

Agents tell us they find this easier too: they're no longer worrying about whether they accidentally wrote down a digit, whether the recording captured something it shouldn't have, or whether they'll be blamed if a customer's card is later compromised. That reduction in anxiety has a real effect on staff retention in a sector where turnover is already painful.

If you want a single metric to track, look at completion rate at the point of payment — the percentage of calls where payment is offered against the percentage where it's actually captured before the customer hangs up. Most customers we work with see this lift after masking goes live. The other useful number is time-to-payment: the days between a service being agreed and the cash arriving. If that drops from weeks to zero because the payment closes on the call, the privacy advantage is doing what it's supposed to.

Where it fits in your stack

We don't rip and replace. You keep your contact center platform, your processor, your CRM, your QA platform, your headsets. We slot into the audio path and change one thing — what reaches the agent during the seconds the customer is keying digits. Everything else carries on as before.

On modern cloud contact center platforms — Five9, NICE CXone, Genesys Cloud, Amazon Connect, RingCentral, Talkdesk, 8x8, 3CX — we connect via API or SIP and the integration is a few hours of work on our side and a sign-off on yours. Traditional PBXes (Mitel, Avaya, Cisco UCM) and plain SIP trunks are the same shape with slightly more coordination on routing.

Your processor can be Stripe, Authorize.Net, Braintree, Worldpay, Adyen, Cybersource, NMI, TSYS, Fiserv or any of the long tail — if it has an API, we talk to it. We support seven integration patterns in total: network-level divert, PBX-level divert, IVR menu, agent transfer or conference, PSTN outbound via Paytia, Paytia WebRTC, and direct SIP trunk integration. Between them, that covers almost every US contact center telephony stack we've walked into.

For the agent, the behavior change is genuinely small — enter the amount, press 729, watch a progress indicator until you see the green light, carry on the conversation. A 15-minute team huddle covers it for most teams.

The bigger piece of work is usually social: deciding how the agent introduces the capture (“I'm going to take your card details now — when you're ready, please enter your card number on your phone keypad and I'll see when you're done”), making sure the script feels natural, and getting team leads comfortable with the new audit trail.

Edge cases that occasionally surface: old softphones with off-frequency DTMF (five-minute tolerance widen on our side), poor cellular signal degrading detection (the retry prompt handles it cleanly), a SIP carrier converting tones to RFC 2833 events (different handler, same outcome), or a recorder forking the stream at the SBC layer rather than the application layer (we just need to confirm masking sits upstream). None of these are projects.

If you want to see how this lands in your specific environment, book a 15-minute demo and we'll map it against your stack. If you'd rather see it side-by-side against the alternative architecture, channel separation takes a different route to the same compliance outcome — the comparison page walks through where each one lands in practice. Or call us on +1 315 716 2226.

Lower

Compliance costs

Significant

Annual audit savings

Zero

Card data in your environment

< 1 Week

Typical setup time

“Paytia helped us turn a security exposure and reputational risk into a value-enhancing opportunity. Fundraising has never been more important, and Paytia helped us hit our goals.”

Cambridge University

Trusted by British American Tobacco · Howard Kennedy · CITB · Clinical Partners · Trinity Hall College

How DTMF Masking Works

Here's what a typical payment looks like, from start to finish.

Customer Calls In

They reach your payment line or your agent transfers them. Voice prompts walk them through — or the agent does, since they're still on the call.

Card Details Entered by Keypad

The customer types their card number, expiration, and CVV on their phone keypad. Paytia masks the tones so nothing sensitive reaches your agent or your recordings.

Payment Confirmed

The transaction goes through in seconds. The customer gets confirmation on the call plus SMS or email, depending on how you've set it up.

What You Get

Everything you need to take secure phone payments, built into one platform.

Tone Masking

Every keypress generates a flat replacement tone. The real card data is captured by Paytia and never reaches your agent or call recording.

Agent-Assisted Payments

Your agent stays on the line while the customer enters their card details. They can help throughout — that's what makes DTMF masking different from a cold IVR hand-off.

24/7 Payment Line

Customers can pay outside business hours too. The IVR handles it — no agent needed for after-hours payments.

Reporting Dashboard

See transaction data, success rates, and where customers drop off. All in one place, updated in real time.

Payment Confirmation

Customers get confirmation by voice on the call, plus email or SMS with a reference number. You pick what fits your process.

Plugs Into Your Stack

Works with your existing CRM, billing system, and payment processor. We handle the integration.

Simplify PCI DSS Compliance

PCI DSS Level 1

Built on infrastructure that meets the highest level of PCI compliance standards. Works alongside HIPAA and TCPA obligations US businesses already carry.

| Requirement | Without Paytia | With Paytia |

|---|---|---|

| PCI Assessment | SAQ D (329 Qs) | SAQ A (22 Qs) |

| Network Security | Extensive | Minimal |

| Call Recording | Complex & Risky | No restrictions |

| Staff Training | Extensive | Minimal |

| Annual Audit Costs | $20,000–$65,000 | $4,000–$10,000 |

DTMF Masking Use Cases

Organizations across every US sector use DTMF masking to take card payments over the phone while protecting customers and simplifying compliance.

Contact Centers

Agents process card payments during calls without ever hearing card data. Works with any contact center platform. Without it, every call recording is a compliance liability — and with TCPA claims on the rise, you don't want extra exposure.

- •Card data stripped from recordings

- •Agents stay connected throughout

- •Works with any platform

See contact center PCI compliance →

Financial Services

Banks, insurers, and lenders collect premiums, deductibles, and loan payments securely over the phone. FINRA, the FTC, and state regulators expect you to protect customer data — delays invite scrutiny.

- •Premium and loan collection

- •FINRA and FTC aligned

- •Reduced PCI scope

Healthcare

Hospitals, clinics, and billing services collect copays and outstanding balances by phone. HIPAA covers PHI, PCI DSS covers card data — DTMF masking keeps both out of your recordings. One breach is catastrophic.

- •Copay and balance collection

- •HIPAA and PCI DSS aligned

- •Breach risk reduction

Nonprofits

Fundraising teams take donations securely without exposing donor card details. Donors trust you with their money — a breach destroys that trust overnight, and recovery is painful.

- •Secure donor payments

- •No card data exposure

- •Trust preservation

Complete Secure Payment Solutions

DTMF masking is one part of what we do. Here are the other ways Paytia helps US businesses take payments securely.

AI CallSynch

Agents stay on the call while customers enter card details securely. Full payment portal with real-time transaction tracking.

Learn more →Payment Links

Send encrypted payment links by email or SMS with Secure Code verification. A strong fit for collections and invoice payments.

Learn more →Click-to-Pay

One-click payment processing from your website or customer portal with fraud detection and 3DS2 verification.

Learn more →PCI DSS Compliance

Reduce your PCI scope from SAQ D to SAQ A. Our platform handles all card data so your systems never touch it.

Learn more →Web Chat Payments

Accept secure payments during live web chat sessions without exposing card data to chat agents.

Learn more →AI Sensitive Data Capture

Securely collect bank details, SSNs, and other sensitive data during phone calls.

Learn more →Comparing approaches

If you're weighing how to take card payments by phone, our side-by-side comparison of DTMF masking and channel separation walks through what each approach asks of your agents, your call recordings, and your auditor.

Frequently Asked Questions

What is DTMF masking and how does it work?+

DTMF masking replaces the audible tones generated when customers press keys on their phone during payment entry, while keeping the agent on the call the whole time. Sensitive card information can't be overheard by anyone nearby, and agents can still answer questions and help throughout the payment. The tones are masked in real time so card data never reaches your recordings or your agent's workstation.

What's the difference between DTMF masking and DTMF suppression?+

Nothing — they're two names for the same technology. Most US contact centers search for DTMF masking, so that's what we lead with. You'll also see it called DTMF suppression in some vendor docs. Both describe intercepting the keypad tones in real time so they never hit your agent's audio or your call recording.

How does DTMF masking reduce PCI DSS compliance scope?+

With DTMF masking in place, your organization can cut its PCI DSS compliance scope significantly. Card data is masked and never audibly transmitted, so the risk of interception is gone. That lets you classify your agent-assisted payment environment as lower-risk, which usually means lower compliance costs and simpler audits while keeping the same level of security and customer interaction.

Can DTMF masking be integrated with existing phone systems?+

Yes. Our DTMF masking works with most existing phone systems and PBX platforms used by US businesses. We support the major telephony providers and can plug into both on-premises and cloud-based systems. Our technical team will review your current setup and work through the integration with your team.

What happens if there's an issue with the DTMF masking?+

Our system includes real-time monitoring and fallback mechanisms. If anything goes wrong, it can switch automatically to alternative secure processing or alert our support team. We provide 24/7 monitoring and support so you're not left waiting when something needs attention.

How do customers receive payment confirmations?+

You've got options. Customers can get immediate verbal confirmation during the call along with a unique reference number, plus an email or SMS if you want. The system connects to your existing customer notification tools so confirmations match how you already communicate.

What are the compliance cost benefits of DTMF masking?+

PCI compliance costs keep moving — new controls, new audit requirements, new segmentation work. With DTMF masking, card data never reaches your systems, which typically drops your scope from SAQ D (329 controls) to SAQ A (22 controls). That means a smaller, more predictable annual compliance bill instead of a growing one.

What privacy concerns does DTMF masking address?+

When customers read card numbers aloud on a call, they can be overheard by colleagues in open-plan offices, family members at home, or people nearby in public spaces. That discomfort drives abandoned transactions and complaints. DTMF masking lets the customer enter card details on their keypad while the agent stays on the line — the digits never enter the audio stream, so there's nothing to overhear.

Is DTMF masking suitable for MOTO payment processing?+

Yes. DTMF masking is built for mail-order/telephone-order (MOTO) payments. It enables card-not-present transactions over the phone by masking the keypad tones in real time — so card data never enters call recordings or agent workstations, while the agent stays on the line to handle the rest of the call.

How does DTMF masking affect call recording and PCI scope?+

Because the keypad tones are masked before they reach the recording layer, call recordings no longer contain card data. That removes the recording system, its storage, and its retrieval tools from PCI scope entirely — historically one of the heaviest compliance burdens on contact centers.

What's the cost of NOT addressing card-privacy concerns on calls?+

Customers who are uncomfortable reading card numbers aloud abandon the transaction, ask to pay later, or go to a competitor. In contact centers we've worked with, uncomfortable phone-payment flows show up as higher abandonment rates and longer handle times. DTMF masking removes the discomfort, which typically improves both.

Still Taking Card Details the Risky Way?

We'll show you exactly how DTMF masking works with your phone system in a quick 15-minute call. No pressure, no sales pitch — just a demo. Call +1 315 716 2226 or book online.

Trusted by US law firms, insurers, healthcare organizations and regulated businesses that can't afford to get compliance wrong. Learn more about Paytia

Related solutions

Other ways to take payments in this channel.