At its core, digital banking is the move away from traditional, branch-based banking to a world where financial services are available anytime, anywhere, right from your computer or mobile device. It takes finance out of the brick-and-mortar building and puts it squarely in the palm of your hand through websites and apps.

From Physical Queues to Digital Clicks#

Think of the old way of banking like visiting a physical library. To get a book, you had to travel there, search the aisles, and wait in line at the counter—all during set opening hours. Digital banking is like having that entire library, plus every book ever written, instantly available on your phone.

This isn't just a small step up in convenience; it's a fundamental change in our relationship with money. Instead of scheduling your day around the bank, your bank now fits around your schedule. It's given both people and businesses a level of control and efficiency that was unthinkable just a decade ago.

The New Standard for Financial Management

UK digital banking adoption has grown sharply. By 2025, around 88% of UK adults were using some form of online banking — roughly 48 million people.

Already, 75% of UK adults rely on mobile banking apps for everyday transactions. This hunger for speed and simplicity has completely reshaped customer expectations, especially for contact centres, where fast digital interactions—including secure payments—are now table stakes. You can find more stats on these trends over on Finder's UK digital banking analysis.

The shift online touches every corner of our financial lives, from simple tasks to complex operations.

- For Individuals — It's checking your balance on the bus, paying a friend back while watching TV, or applying for a loan without ever leaving your house.

- For Businesses — It's taking customer payments instantly, managing payroll from a single dashboard, and automating account reconciliation.

Digital banking isn't just a technology upgrade — it changes the customer relationship. Services are expected to be available on demand, not tied to branch hours.

Exploring the Core Types of Digital Banking#

Digital banking isn't a single, monolithic thing. Think of it more as an ecosystem with different branches, each designed for a specific job. Getting to grips with these different forms is the key to understanding how modern finance really works.

Each one offers a distinct way to manage money, whether it's a quick tap on your phone to pay a friend or a sophisticated portal for managing a company's finances. Let's break down the four main pillars of the digital banking world. While they often overlap and work together, they each serve a unique purpose.

Mobile Banking: The App in Your Pocket

When most of us hear "digital banking," this is what we picture: managing finances through a dedicated app on a smartphone or tablet. It's all about speed, convenience, and getting things done on the move.

Paying a bill while waiting for the train or sending money to a friend from a café – these are the moments where mobile banking shines. For businesses, this opens up powerful new ways to interact with customers. A contact centre agent, for example, could send a secure payment link directly to a customer's phone, letting them pay instantly without having to read out card details.

The whole experience is fine-tuned for a small screen, focusing on the tasks you do most often:

- Checking Balances — A real-time snapshot of your accounts.

- Making Payments — Settling bills or paying people quickly.

- Transferring Funds — Moving money between your own accounts in seconds.

- Depositing Cheques — Using your phone's camera to deposit a cheque without visiting a branch.

Online Banking: The Full Web Portal

Online banking is the web-based big brother to mobile banking, typically accessed through a browser on a laptop or desktop. Where mobile banking is about quick, simple tasks, online banking provides a more powerful and detailed platform for deeper financial management. It's less about speed and more about depth and control.

For instance, a small business owner wouldn't use a mobile app to manage their monthly payroll. They'd log into their bank's online portal to access advanced features like bulk payments, download detailed transaction histories, and use sophisticated reporting tools. It's the tool for the heavy lifting.

Online banking is where most business users do the detailed work — bulk payments, payroll, transaction reporting.

Neobanks: The Digital-Only Challengers

Neobanks are a complete rethink of what a bank can be. These are banks that exist entirely online, with no physical branches to visit. You've probably heard of names like Starling Bank, Monzo, and Revolut in the UK. By ditching the huge overheads that come with running brick-and-mortar locations, they can often offer lower fees, better interest rates, and a user experience built from the ground up for a digital-native audience.

Their whole focus is on creating an intuitive mobile experience. They often build in budgeting tools, spending analytics, and easy-to-use savings features right into their apps. These digital-first players are forcing traditional banks to up their game and innovate much faster.

Open Banking: The Connected Financial Ecosystem

This is perhaps the biggest shift in banking in a generation. Open Banking is a regulatory-driven movement that lets you securely share your financial data with trusted third-party providers. It all works through Application Programming Interfaces (APIs), which are essentially secure channels that allow different software systems to talk to each other.

Imagine linking your bank account to a budgeting app that automatically sorts your spending, or to a service that scans all your accounts to find you a better mortgage deal. That's Open Banking in action. It puts you in control of your own financial data. It also paves the way for new payment methods, allowing you to pay a business directly from your bank account through a licensed provider. You can learn more about how this connects to other payment methods in our guide on what is a digital wallet.

Together, these four pillars create a flexible and powerful financial world, offering the right tool for every job—from a simple mobile payment to a deeply integrated financial management system.

Want to see this working in your setup? Book a working-demo call — we'll wire up your actual phone system and show you a live capture.

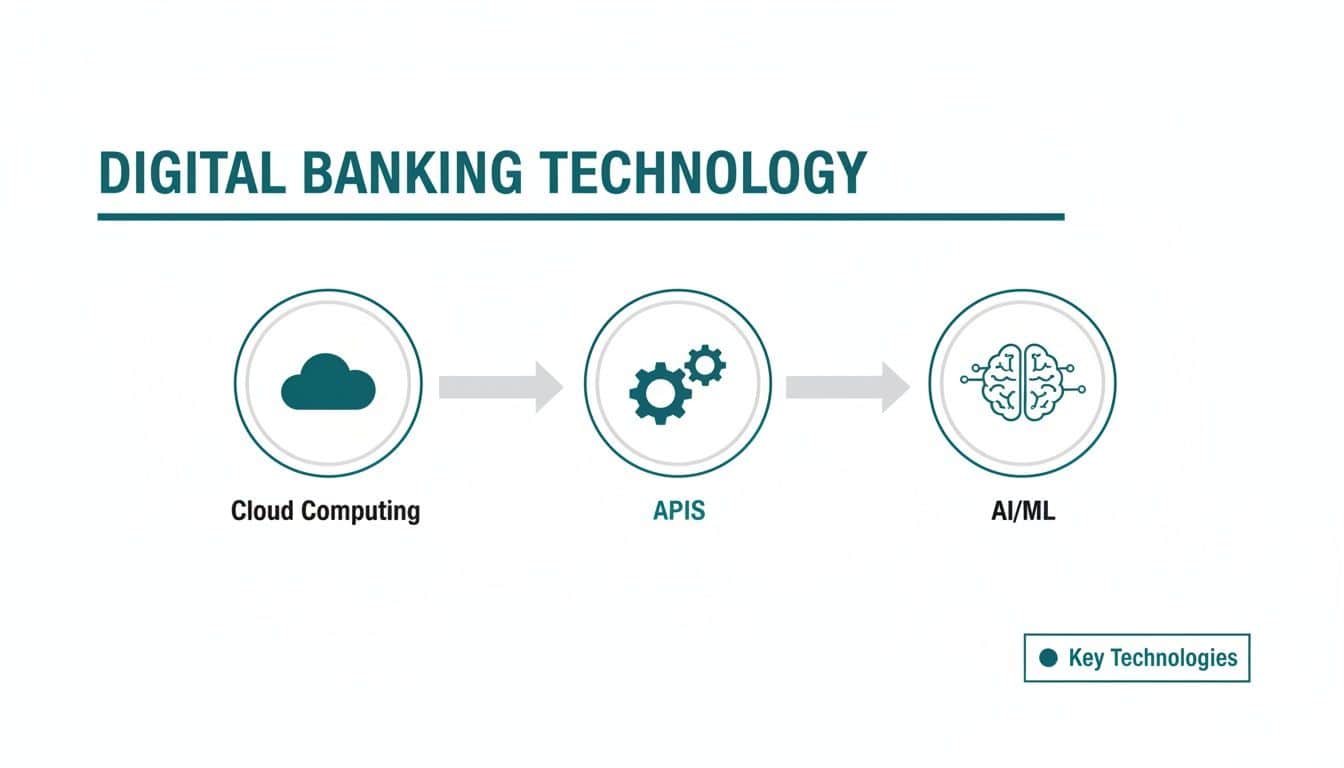

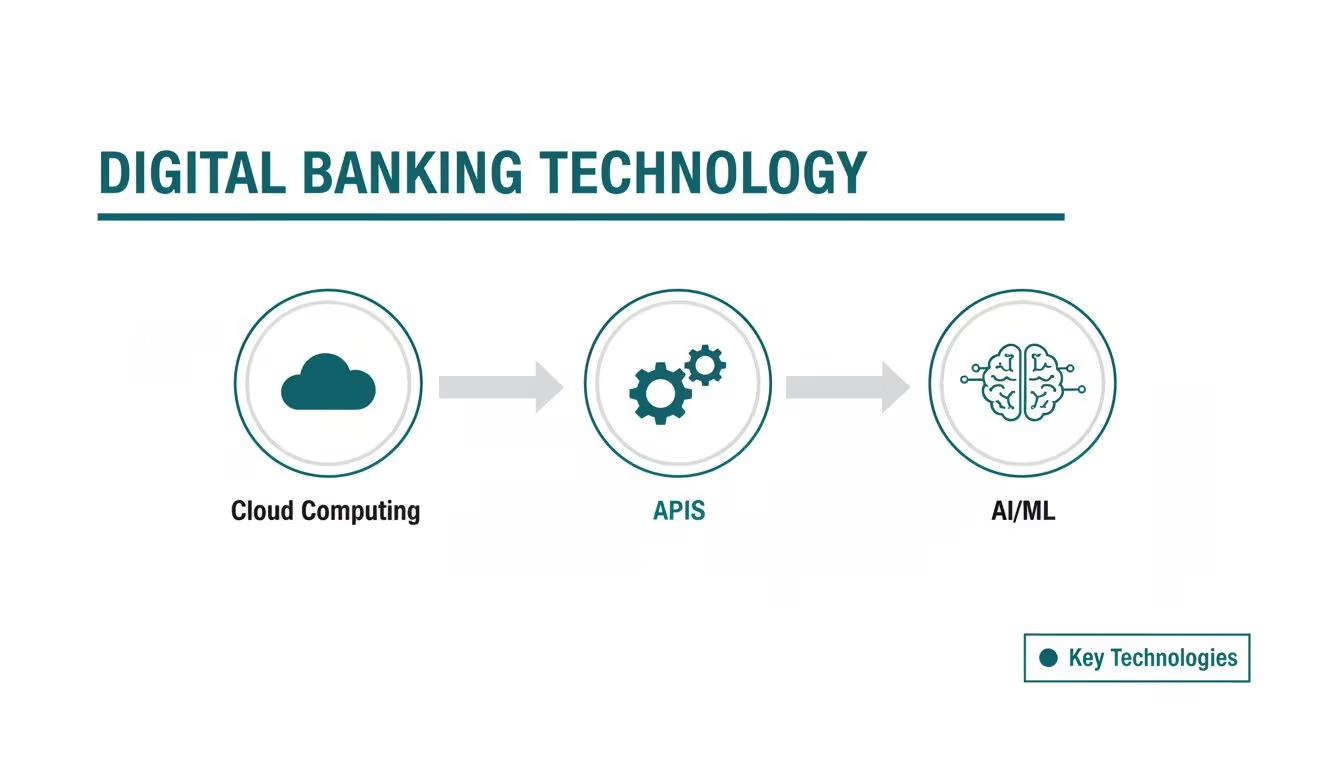

The Technology Powering Modern Finance#

To really get what digital banking is, we need to look under the bonnet. Behind the slick apps and instant transfers, there's a powerful mix of technologies working together. This isn't just about lines of code; it's about a fundamental shift in how financial services are built, delivered, and secured.

At the heart of it all are a few key advances that act as the engine room for modern finance. They provide the flexibility, connectivity, and intelligence needed to create the fast, reliable experiences we've all come to expect. Let's break down the tech that makes it all happen.

The Foundation of Flexibility: Cloud Computing

In the old days, banks relied on massive, expensive servers sitting in their own data centres—a bit like having a huge power generator in your house. It was powerful, sure, but also rigid, costly to maintain, and a nightmare to upgrade. Cloud computing changes the game entirely, letting banks rent computing power and storage from providers like Amazon Web Services or Microsoft Azure.

This move to the cloud gives them incredible scalability. During a busy period, like the end of the financial year, a bank can instantly scale up its resources to handle the flood of transactions. When things quieten down, it can scale back down just as quickly. This elasticity means they only pay for what they use, which saves a fortune and boosts efficiency.

More importantly, it lets them move much faster. New features and critical security updates can be rolled out in hours instead of months. For modern digital banking platforms, keeping things running well and handling high transaction volumes is non-negotiable. You can learn more about boosting application performance through load testing to see how these systems are stress-tested for resilience.

The Language of Connectivity: APIs

If cloud computing is the foundation, then Application Programming Interfaces (APIs) are the translators that let different systems talk to each other. Think of an API like a waiter in a restaurant. You (the user) don't need to march into the kitchen (the bank's core system) to place your order.

Instead, you give your request to the waiter (the API), who relays it to the kitchen and brings the food back to you. This is exactly how Open Banking works. An API lets your budgeting app securely ask for your transaction history from your bank, without either system needing to know the messy inner workings of the other.

This connectivity is vital for creating integrated financial ecosystems. It allows businesses to link their accounting software directly to their bank accounts or to use solutions like Paytia to offer secure, real-time payment options such as a Pay by Bank request.

APIs are what let different financial systems talk to each other without either having to understand the other's internals.

The Brains of the Operation: AI and Machine Learning

The final key ingredient is intelligence, and that's where Artificial Intelligence (AI) and Machine Learning (ML) come in. These technologies are the brains of the operation, constantly sifting through massive amounts of data to make digital banking smarter, safer, and more personal.

Their impact is felt across several critical areas:

- Fraud Detection — AI algorithms can analyse thousands of transactions a second, spotting unusual patterns that scream "fraud" in real-time—often stopping theft before it even happens.

- Personalised Experiences — By understanding your spending habits, AI can offer tailored financial advice, suggest savings goals, or recommend products that are actually useful to you.

- Customer Service — AI-powered chatbots can handle common questions 24/7, freeing up human agents in a contact centre to deal with more complex problems that need a human touch.

Together, these technologies form a powerful trio. The cloud provides a flexible foundation, APIs create the connections, and AI adds the intelligence that makes digital banking not just possible, but a genuinely better experience.

Securing Transactions in a Digital World#

The convenience of digital banking is brilliant, but it's all built on a foundation of trust. Customers need to know their money and personal data are safe. For any business taking payments, security isn't just a nice-to-have feature—it's the bedrock of your reputation and a fundamental responsibility.

Moving money online introduces new risks, but it also brings incredibly powerful security measures to the table, often far stronger than traditional methods. Getting a handle on these safeguards is important for anyone operating in the digital economy.

The diagram below shows the core technologies that don't just power digital banking, but are also central to keeping it secure.

This shows how things like Cloud Computing, APIs, and AI fit together, creating a solid infrastructure where security can be woven into every single layer.

The Essential Layers of Digital Security

Protecting financial data demands a multi-layered approach, where each defence backs up the others. Think of it like a medieval castle: you have strong outer walls, a guarded gate, and secure inner chambers. In digital banking, we build these layers with clever technology.

First up is full encryption. This basically acts like an unbreakable, sealed envelope for data as it travels from a customer's device to the bank's servers. Even if someone managed to intercept it, all they'd get is scrambled, unreadable code.

Next, we have tokenization. This is a smart process that swaps out sensitive data, like a full 16-digit card number, for a unique, non-sensitive stand-in called a "token." The actual card details are locked away securely somewhere else, far from the transaction itself. If a breach happens, the thieves only make off with worthless tokens, not real card numbers.

Finally, Multi-Factor Authentication (MFA) stands guard at the gate. It makes customers prove their identity with more than just a password—maybe a code sent to their phone or a quick fingerprint scan. This one simple step blocks the vast majority of attempts to gain unauthorised access.

Getting PCI DSS Compliance Right

If your business accepts, processes, or stores cardholder information, there's one set of rules that matters more than any other: the Payment Card Industry Data Security Standard (PCI DSS). This is the gold standard for payment security. Failing to comply can lead to serious penalties, including hefty fines and even losing the ability to take card payments altogether.

Before mobile apps took over, most customers relied on telephone banking to check balances and move money.

The same shift is fuelling voice commerce, where customers order and pay through voice assistants or phone calls.

Getting and staying PCI DSS compliant can be a huge job. It means implementing rigorous security controls, running regular network scans, and undergoing detailed audits. The cost and complexity can be a real burden, especially for places like contact centres where payment details are often spoken over the phone.

This is where modern payment solutions make a massive difference. They are built specifically to shrink a company's PCI DSS scope.

By using technologies that stop sensitive card data from ever entering your business environment in the first place, you can offload a huge chunk of the compliance burden. This not only saves money but also dramatically lowers the risk of a data breach.

Securing Voice Payments in the Contact Centre

Contact centres are a classic example of a high-risk environment. When a customer reads their card number over the phone, that data can easily end up on call recordings or an agent's screen, instantly dragging the entire infrastructure into the scope of PCI DSS.

This is where a technology called DTMF (Dual-Tone Multi-Frequency) suppression becomes absolutely essential. Here's a look at how it works:

- Secure Handover — When it's time to pay, the agent kicks off a secure payment process. The customer is then asked to type their card details using their phone's keypad.

- Masking the Tones — As the customer enters their details, the DTMF tones are masked. The agent just hears a flat, unrecognisable tone and sees asterisks on their screen instead of numbers.

- Direct to Gateway — The sensitive data completely bypasses the contact centre's systems and goes straight to the payment gateway for authorisation.

This process ensures the Primary Account Number (PAN) and CVC never touch the business's network or get saved in call recordings. The result? A massive reduction—often up to 90-95%—in PCI DSS scope. It saves time, money, and a lot of headaches, all while building huge trust with your customers.

How Digital Banking Changes the Contact Centre#

The technology driving digital banking does far more than just power up your personal finance apps. It has a massive ripple effect on core business operations, and nowhere is that more obvious than in the contact centre—the very crossroads of customer interaction and financial transactions.

Not long ago, the contact centre was seen mainly as a support function, a place customers called when something went wrong. That view is changing fast. Thanks to the integration of digital banking and payment technology, it's now becoming a secure and highly effective revenue channel.

These advances help both agents and customers, turning what could be awkward payment conversations into secure, professional experiences. Let's look at a few real-world applications making this happen right now.

Agent Assisted Payments Made Simple and Secure

Picture a customer calling to pay an overdue bill. In the old days, this involved the uncomfortable and high-risk process of them reading their card details out loud. The agent would then have to manually key that sensitive information into a system, creating a huge security and compliance headache.

Digital banking flips this scenario on its head. Using modern secure payment platforms, an agent can kick off the payment process while staying on the line to guide the customer. The customer simply enters their details using their telephone keypad, while DTMF masking technology ensures the tones are completely hidden from the agent and the call recording.

This one simple change solves several critical problems at once:

- Improved Security — Sensitive card data never even touches the contact centre's environment, which dramatically reduces the risk of a breach.

- Boosted Customer Trust — Customers feel much safer knowing their private financial details are never spoken aloud or seen by another person.

- Simplified Compliance — The business shrinks its PCI DSS scope massively, saving a huge amount of time and money on audits and controls.

Expanding Payment Channels for Modern Customers

Customer expectations have never been higher, and they now demand flexibility in how they pay. Digital banking allows contact centres to move beyond phone-only payments and offer a whole suite of secure options that fit different preferences.

Just look at how open banking and mobile payments are reshaping UK financial habits. Open banking usage has grown substantially in the UK since the regulations came into force, and mobile banking is now the default channel for most UK adults. Faster Payments volumes continue to grow alongside.

This fundamental shift means contact centres have to offer more than just one way to pay.

- Secure Payment Links — An agent can instantly send a payment link via SMS or email, letting the customer complete the transaction on their own device.

- Automated IVR Payments — For simple, recurring payments or out-of-hours collections, customers can use an automated Interactive Voice Response (IVR) system to pay 24/7 without speaking to anyone.

- Web Chat Payments — Secure payment fields can be embedded right inside a web chat window, allowing an agent to collect a payment during a live text conversation.

Integrating these channels turns the contact centre from a single-channel support function into a multi-channel collection operation.

The integration of these tools is central to creating modern, effective customer service operations. To understand how artificial intelligence is specifically improving customer interactions in the financial sector, a complete guide on AI in banking customer service can provide valuable insights.

Ultimately, this digital evolution is about more than just technology. It's about building a more efficient, secure, and customer-focused operation that can adapt to ever-changing financial behaviours. This is a key focus for businesses implementing cloud-based contact centre solutions designed for the modern economy.

Your Digital Banking Implementation Checklist#

Moving from theory to practice is where things get real. For any business, especially contact centres, bringing in new digital banking and payment tools needs a proper plan. This checklist gives you a clear, step-by-step framework to follow, making sure your implementation is both secure and successful.

Think of it less like a technical project and more like building a bridge of trust with your customers. Each step is designed to make that bridge stronger, safer, and easier for payments to travel across.

Step 1: Audit Your Current Channels

Before you build anything new, you need a map of the existing territory. Start by taking a detailed inventory of every single channel you use to take payments—whether that's over the phone, on your website, or anywhere else.

For each one, you have to ask the tough questions. Where does sensitive payment data actually flow? Is it spoken aloud? Typed into a screen? Saved in call recordings? Pinpointing these security weak spots is the absolute first step to cutting down your risk.

Step 2: Define Your Security and Compliance Needs

Once you have a clear picture of where you are, you can decide where you need to go. This is where you map out your specific security and compliance duties, with a laser focus on your Payment Card Industry Data Security Standard (PCI DSS) scope.

Your main goal here should be to shrink that scope as much as possible. A solution that stops sensitive card data from ever touching your environment is the gold standard. Getting these needs clearly defined will be your guide when you start looking at different technology partners.

Step 3: Choose a Secure Payment Platform

Now it's time to pick the right tools for the job. You'll want to find a secure payment platform that doesn't just tick your security boxes but also fits neatly with the systems you already use, like your telephony and CRM software.

The right platform handles payments efficiently without adding confusing steps or security gaps.

Look for platforms that offer a range of tools like DTMF suppression for phone payments, secure digital payment links, and automated IVR options. This flexibility means you can cater to how different customers prefer to pay.

Step 4: Design a Clear and Trustworthy Experience

Technology is only half the story. The experience you create for both your agents and your customers is just as critical. A clunky, confusing payment process kills trust and often leads to customers giving up halfway through.

Focus on building a workflow that feels professional and completely transparent. Agents need to feel confident walking customers through the process, and customers need to feel secure at every turn. This comes down to clear instructions, simple interfaces, and reassuring security prompts that show their data is being handled properly.

Step 5: Establish Solid Monitoring and Reporting

Finally, a successful rollout doesn't end at launch—it needs constant oversight. Set up solid processes for monitoring transactions, reporting on how things are going, and running regular internal checks. This is how you stay compliant and spot any issues or areas for improvement quickly.

The platform you choose should give you detailed, audit-ready reports that offer full visibility into all payment activity. This continuous feedback loop is vital for keeping your digital payment environment secure and efficient, giving your organisation total confidence in its financial operations.

Your Digital Banking Questions Answered#

In short, let's tackle some of the most common questions people have when they're getting to grips with digital banking. These quick-fire answers should help cement the key ideas we've covered and clear up any lingering practical concerns.

Is Digital Banking Actually Safe?

Yes, absolutely—when it's done right. Proper digital banking platforms aren't just regular systems with a bit of security sprinkled on top; they are built from the ground up with multiple, layered protections. This makes them exceptionally secure for both you and your customers.

Think of it like a bank vault with several different locks. Key security measures usually include:

- Full encryption, which scrambles data so it's completely unreadable to anyone who might intercept it.

- Tokenization, a clever process that swaps sensitive card numbers for non-sensitive, placeholder "tokens."

- Multi-Factor Authentication (MFA), which demands more than just a password to prove you are who you say you are.

When you combine these protections, digital transactions often end up being far more secure than many traditional, offline methods.

What's the Real Difference Between Online and Mobile Banking?

It's a good question, as the two are closely related. The easiest way to think about it is comparing a detailed car dashboard to a quick-glance smartphone widget. Both give you information, but for different situations.

Online banking is what you access through a web browser on a laptop or desktop. It's the full experience, offering a wide range of tools for deep-looking at your finances, running reports, or handling complex tasks.

Mobile banking, on the other hand, is all about the dedicated app on your phone. It's designed for speed and convenience, prioritising the things you need to do on the move, like checking a balance, pinging a quick payment, or freezing your card.

How Does PCI DSS Fit into Digital Banking?

The Payment Card Industry Data Security Standard (PCI DSS) is the rulebook for any business that accepts, processes, stores, or even just transmits card details. If a digital banking platform handles card payments in any capacity, then PCI DSS compliance isn't just a good idea—it's non-negotiable.

For contact centres specifically, choosing a provider that is itself PCI DSS Level 1 certified removes most of the compliance burden from your own environment.

Related reading#

- Pillar guide: Payment Gateway API Integration: 2026 Developer Guide

- Pay by Link vs Hosted Checkout: Which to Use

- Manual vs Automated Payment Chasing: When to Switch

- How Open Banking Works: Essential Business Guide

- What is click to pay: A Faster, Safer Online Checkout

Want to see this working in your setup? Book a working-demo call — we'll wire up your actual phone system and show you a live capture.