Admin Portal

Platform features in context

Manage telephone numbers, users, campaigns, and payment capture from the Paytia admin — built for contact center scale and flexible licensing.

Manage Telephone Numbers

Buy and activate numbers in real time; set call presentation and SIP calling per number.

Users and Roles

Set up unlimited agents; pay only when a user takes a payment. Free administrative licenses included.

Data Capture and Forms

Configure payment and customer fields per campaign — flexible customization for each client objective.

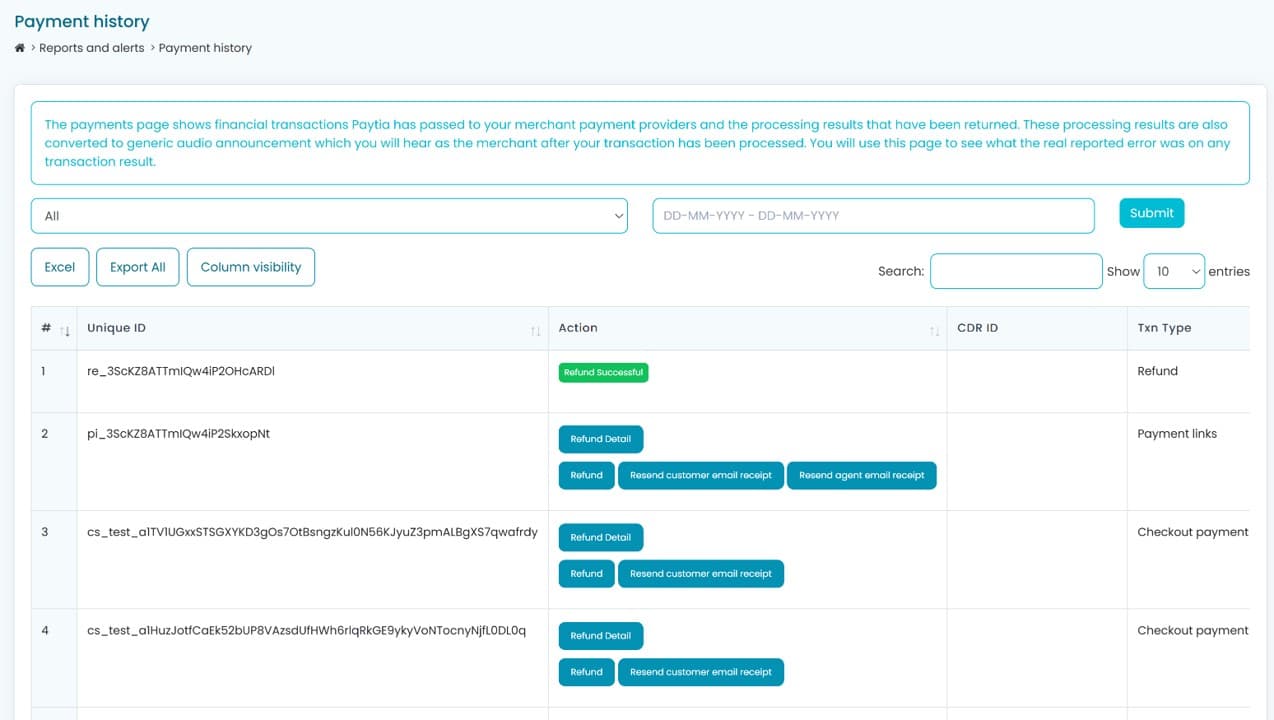

Payment History and Reports

Search transactions, run refunds, and export payment history — all without exposing card data to your team.

Agent Capture Assist

Agent Capture Assist

Customer Lookup

Users can retrieve customer records in real-time directly from the Paytia user interface.

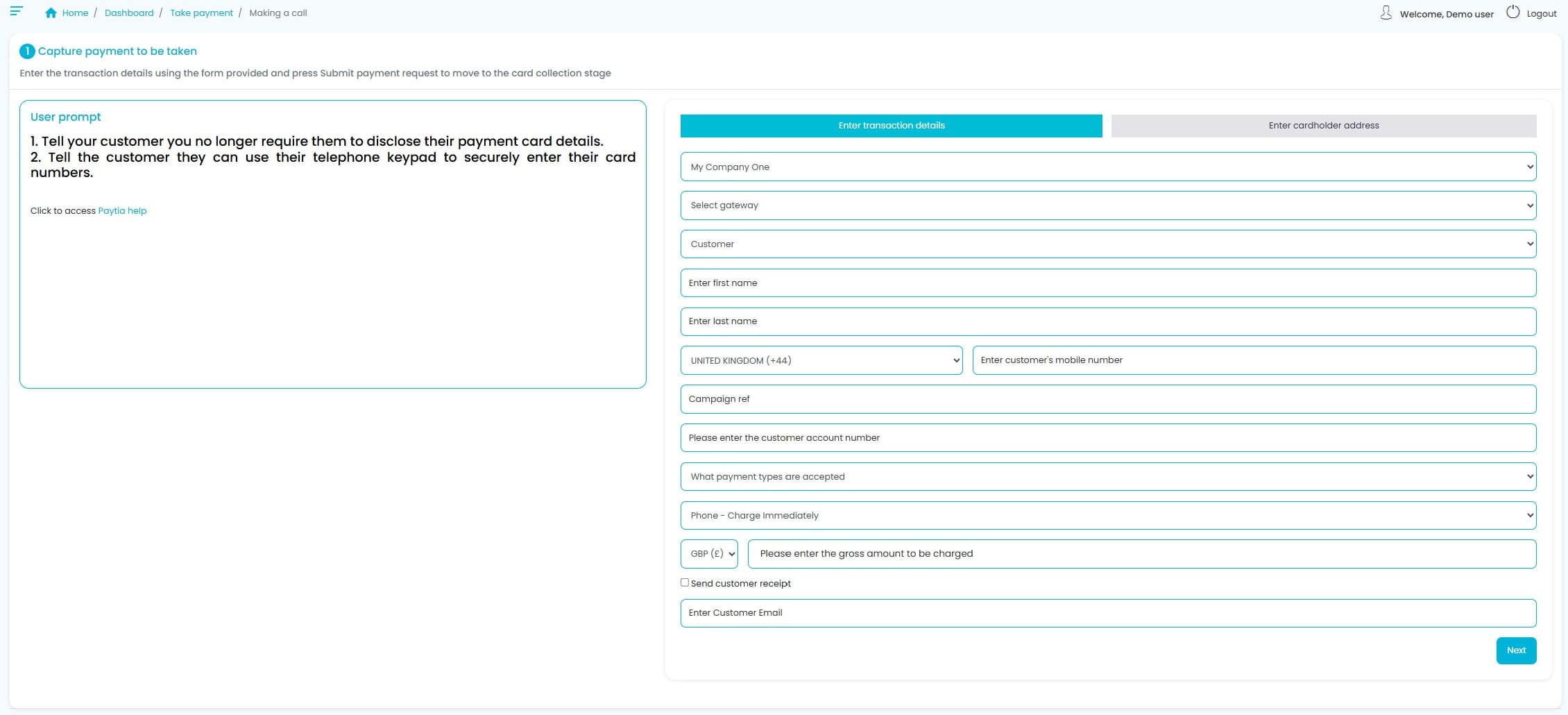

Transaction Start Capture

Start a secure capture from the Paytia user interface — card details stay off the call and out of your systems.