In the world of payments, the term Primary Account Number (PAN) refers to that long string of digits on the front of your credit, debit, or prepaid card. It's the unique identifier for your payment account, typically 16 digits long, though it can sometimes be as many as 19.

But this number is much more than just a random sequence; it's a structured code packed with vital information.

The Anatomy of a Primary Account Number#

It helps to think of a PAN not as a single number, but as a detailed address. Just as a physical address has a country code, a city, a street, and a house number, a PAN has distinct parts that route payment information correctly and securely.

This number is the key that unlocks the global payments network, making sure funds are pulled from the right account and sent to the right merchant. This intelligent design is the bedrock of how trillions of pounds in transactions are processed every year, with each segment of the PAN playing a specific role.

Breaking Down the Digits

The structure of a PAN is standardised by the International Organisation for Standardisation (ISO). While the exact length might change from card to card, the core components stay the same.

Here's how a typical 16-digit PAN breaks down:

- Major Industry Identifier (MII) — The very first digit tells you the card network. For example, a '4' means it's a Visa card, while a '5' points to Mastercard. It's the first clue in the routing puzzle.

- Issuer Identification Number (IIN) — The first six to eight digits, including the MII, make up the IIN. This sequence identifies the specific bank or financial institution that issued the card.

- Individual Account Identifier — These are the digits that follow the IIN. They uniquely identify the individual cardholder's account within the issuing bank's system.

- Checksum Digit — The final digit isn't random—it's calculated using the Luhn algorithm, a simple formula used for validation. This single digit acts as a important error-checking tool to catch typos and basic fraud during manual entry. You can learn more about this in our complete guide to payment validation techniques.

A Primary Account Number isn't just a number; it's a map. It provides the precise coordinates for a financial transaction, directing information from the card network, to the issuing bank, and finally to the specific customer account.

This structured approach is what allows a transaction request to be instantly routed to the correct financial institution for authorisation the moment a card is used.

To make this clearer, let's break down a sample 16-digit Visa card number into its components.

Anatomy of a Primary Account Number (PAN)

| Component | Digit Position | Description | Example (Visa Card) |

|---|---|---|---|

| Issuer Identification Number (IIN) | Digits 1-6 | Identifies the card network and the issuing bank. The first digit is the MII. | 453215 |

| Individual Account Identifier | Digits 7-15 | Uniquely identifies the cardholder's account. | 123456789 |

| Checksum Digit | Digit 16 | Validates the number using the Luhn algorithm to catch errors. | 0 |

Getting your head around this structure is the first step toward appreciating the security measures built into the payments ecosystem. Every time a card is swiped, tapped, or entered online, this intricate string of numbers performs its role silently and efficiently, making modern commerce possible.

Tracing a PAN Through a Live Transaction#

Knowing the structure of a Primary Account Number is one thing, but seeing it in action is where the real risks become clear. Think of the PAN as a securely sealed package. The moment a customer shares it, that package starts a lightning-fast journey across the complex payments network.

Let's walk through a common scenario: a customer calls your contact centre to pay a bill. They read out their 16-digit card number to your agent. Right there, the PAN has entered your business environment, and its journey—along with all the associated security headaches—has officially begun.

The agent keys the PAN into your payment software or CRM. That data is now live, moving from their keyboard, across your internal network, and out towards the payment processing world. Every single step is a potential weak point if not properly locked down.

The Initial Handoff

Once submitted, the transaction data, led by the PAN, is fired off to your payment gateway. This gateway is like a secure sorting office, checking the initial details before sending the package on its way. It encrypts the data and routes it through the correct card network (like Visa or Mastercard) to the customer's own bank for approval. Our article on payment gateway API integration dives deeper into how this connection works.

This entire back-and-forth happens in just a few seconds, but in that time, the PAN has already touched multiple systems. The issuing bank confirms the funds are available, runs a few security checks, and sends back a simple 'approved' or 'declined' message. That response travels all the way back along the same path, closing the transaction loop.

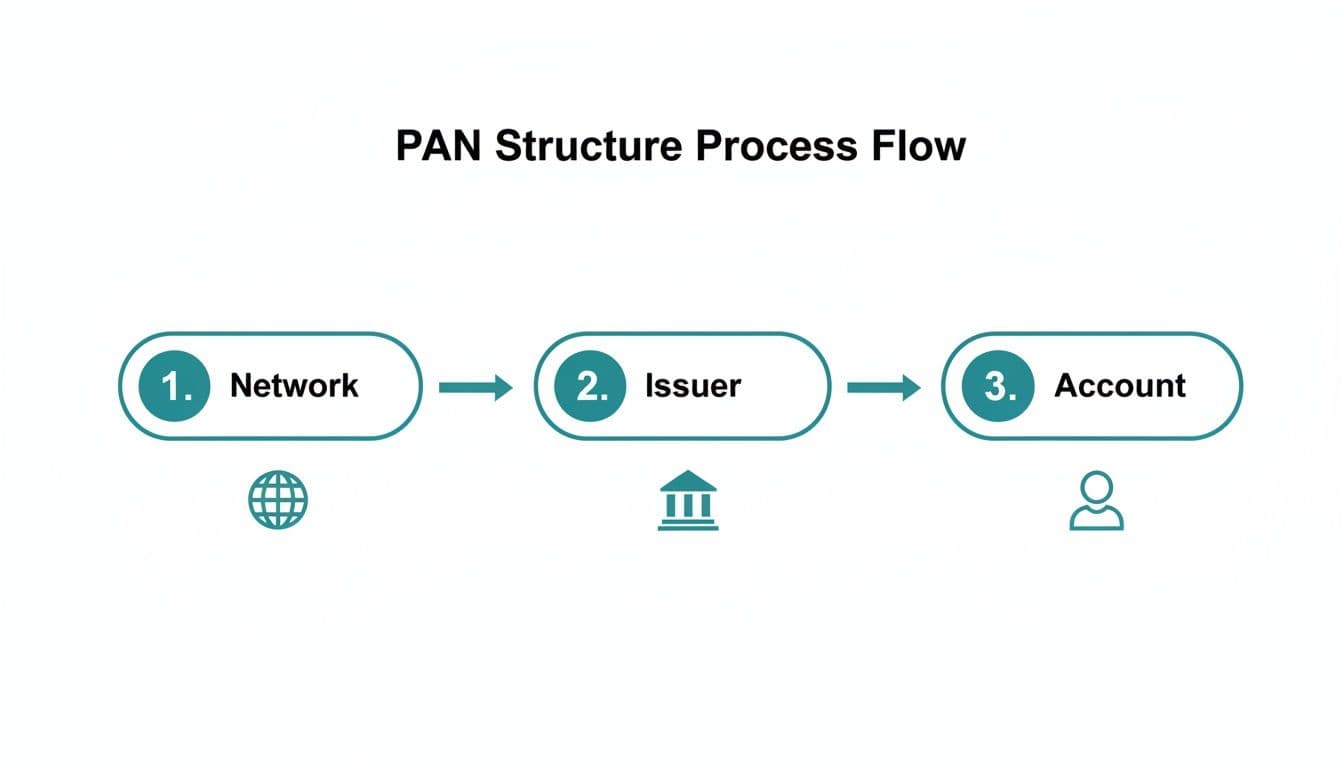

This infographic gives you a high-level look at how the PAN acts as the bridge between the card network, the issuing bank, and the customer's account.

As you can see, the PAN is the central key. It's what unlocks the communication between the global card networks and the specific bank holding your customer's money.

Identifying the Danger Zones

While the journey outside your business is heavily encrypted and regulated, the biggest risks are often lurking inside your own four walls. These "danger zones" are the points where PAN data is most vulnerable, creating massive compliance and security challenges.

These weak spots usually pop up in everyday business processes that were never built with payment security in mind. Pinpointing where they are is the first step to fixing them.

The greatest threat to PAN data isn't always a sophisticated external attack. More often, it's the unintentional exposure within internal systems and processes that are not adequately secured for handling sensitive payment information.

Here are the most common places a PAN can be exposed in a contact centre:

- Call Recordings — If you record calls for training or quality control, the customer's spoken PAN gets captured and stored right in the audio file. That's a huge security red flag.

- Agent Desktops — An agent might quickly jot the number down in a digital notepad or an unsecured document, leaving the PAN saved on their local machine or a shared drive.

- CRM and Ticketing Systems — Typing card details directly into customer notes or ticket fields in a CRM often stores the PAN in plain text, making it visible to anyone with access.

- Unencrypted Network Traffic — If your internal network isn't fully secure, the PAN could be intercepted as it travels from the agent's computer to your payment system.

Each of these points represents a failure to protect sensitive data and dramatically increases the scope of your PCI DSS obligations. By understanding these internal weak points, you can start to see why simply taking a payment is far more complex than it seems. The real challenge is doing it without letting the PAN ever touch these high-risk areas.

Curious how Paytia fits in? Have a quick chat with us — we'll show you in 15 minutes whether we're a fit.

The High Cost of Exposing PAN Data#

What happens when a Primary Account Number, or PAN, falls into the wrong hands? It's not just a simple IT headache. The consequences ripple through the entire business, creating a tidal wave that can destabilise a company from the inside out. This isn't theoretical; it's a tangible, expensive reality that hits your finances, your reputation, and your day-to-day operations hard.

Let's picture a mid-sized e-commerce company. They record all their customer service calls for quality assurance, which is standard practice. But an unnoticed vulnerability in their call recording software leads to a massive breach, exposing thousands of PANs that customers read aloud over the phone. The fallout is immediate, catastrophic, and spreads across three distinct but deeply connected areas of damage.

The Immediate Financial Bleeding

The first and most direct hit from a PAN data breach is financial. The bills start piling up almost instantly, kicking off with hefty penalties from the payment card brands for failing to comply with the Payment Card Industry Data Security Standard (PCI DSS).

But those fines are just the opening act. The company will almost certainly face:

- Forensic Audits — They'll be forced to hire expensive external auditors to dig into the breach, pinpoint the source, and figure out just how bad the data compromise really is.

- Fraud Losses — Any dodgy transactions made with the stolen PANs can lead to a mountain of chargeback liabilities and direct financial losses.

- Increased Transaction Fees — After a breach, acquiring banks often hike up a merchant's transaction fees because they're now seen as a higher risk. This eats directly into the profit margin of every single future sale.

For the company in our example, the initial fines alone hit six figures. The forensic audit added another £50,000 to the tab before they even started counting the cost of customer fraud. That's the brutal, upfront price of letting a PAN slip through the cracks.

The Lasting Damage to Your Reputation

While the financial costs are immediate, the damage to your reputation is often more poisonous and much longer-lasting. Trust is everything. A data breach is one of the quickest ways to burn it to the ground. Customers who trusted you with their payment details feel betrayed and vulnerable.

This collapse of trust shows up in a few painful ways:

- Customer Churn — A huge chunk of customers will simply walk away and stop doing business with a company after a breach. They're just not willing to risk their financial security again.

- Negative Publicity — Data breaches are big news. The resulting negative press and social media storm can permanently tarnish a brand's image.

- Trouble Finding New Customers — The public record of a breach makes potential new customers think twice before handing over their payment details, strangling growth for years.

"A data breach is like a fire. The initial financial damage is the blaze itself, but the smoke—the loss of customer trust and brand reputation—can linger for years, choking future growth and opportunity."

Our story's company saw a 25% drop in customer retention in the quarter after they announced the breach. The public fallout forced them into an expensive PR campaign just to stop the bleeding—money that brought in zero new business but was absolutely essential for survival.

The Gamble of Outdated Security Methods

This kind of devastating breach often comes down to one thing: relying on outdated and flawed security practices, especially in contact centres. The most common culprit is the 'pause and resume' method for call recordings, where an agent is supposed to manually stop the recording when a customer shares their PAN and then start it again.

This method is a high-stakes gamble. It banks on flawless execution from both people and technology, every single time. An agent might forget to hit 'pause'. They might pause too late or resume too early. A slight system lag could keep the recording running for just a few important seconds. This single point of failure is all it takes to capture a PAN and create a toxic data asset you never wanted.

Ultimately, protecting a PAN means keeping it out of your systems altogether. Methods like 'pause and resume' only pretend to solve the problem while leaving the door wide open for human error and system failure—a risk that, as our example shows, no business can afford to take.

Understanding PANs and PCI DSS Compliance#

Now that we've tracked the journey of a Primary Account Number (PAN) and seen just how costly a data breach can be, it's time to talk about the rulebook that governs its protection: the Payment Card Industry Data Security Standard (PCI DSS).

This entire standard exists for one core reason—to keep cardholder data safe, with the PAN sitting right at the centre of it all.

While PCI DSS can seem intimidating at first glance, its goal is pretty simple. It sets out the technical and operational rules for any business that accepts, processes, stores, or transmits card information. The second a PAN enters your systems, those rules kick in and apply directly to you. In the UK, where card payments are king, following these standards isn't just a good idea; it's a basic requirement for doing business.

Defining Your PCI Scope: The Quarantine Zone

If there's one concept that trips people up, it's 'PCI scope.' The easiest way to think of it is like a quarantine zone.

Everything inside this zone—every person, every process, and every piece of technology that touches PAN data—has to follow the strict security controls of PCI DSS.

This isn't just about your payment gateway. It includes:

- The agent on the phone hearing the PAN.

- The computer they use to type it in.

- The network carrying that sensitive data.

- The server where the call recording might be stored.

The bigger your quarantine zone, the more complicated, expensive, and time-consuming your compliance becomes. Every single system inside it needs to be locked down, monitored, and audited, which can be a massive drain on resources. The real secret to simpler compliance is to make this zone as small as humanly possible.

The most effective way to manage PCI DSS compliance is to shrink your scope. By preventing PAN data from ever entering your business environment, you drastically reduce the size of your 'quarantine zone,' making security simpler and more affordable.

This is where smart strategy comes into play. If your agents never hear, see, or handle the PAN, they fall outside the scope. If your call recording software never captures it and your CRM never stores it, those systems are also removed from the quarantine zone. This is the foundation of modern, secure payment handling.

Key PCI DSS Rules for Protecting PANs

The full standard is lengthy, but a few key requirements are aimed squarely at protecting the PAN. Understanding them makes it crystal clear why keeping this data out of your environment is so important. For a deeper look at the specifics, this PCI DSS compliance guide is a great resource.

Two of the most critical rules are:

- Requirement 3: Protect Stored Cardholder Data This one is non-negotiable. It states you must not store sensitive authentication data after a transaction is authorised. If you absolutely have to store the PAN, it must be rendered unreadable through methods like truncation, tokenisation, or heavy-duty cryptography. Storing a full PAN in a call recording or a CRM note is a direct violation.

- Requirement 4: Encrypt Transmission of Cardholder Data Whenever PAN data travels across open, public networks (like the internet), it must be encrypted. This is what stops criminals from snatching the data as it moves from your business to the payment processor.

These rules underline the huge responsibility that comes with handling PAN data. Get it wrong, and you're not just putting your customers at risk of fraud—you're exposing your business to serious penalties.

By using technologies that stop the PAN from entering your systems in the first place, you neatly sidestep many of these complex rules. After all, you can't mishandle data you don't have.

This approach simplifies your entire security posture, letting you focus on what you do best instead of constantly managing a sprawling quarantine zone of sensitive data. For a complete overview of how to achieve and maintain these standards, check out our complete PCI compliance guide.

Modern Strategies for Securing PANs#

Once you grasp the immense risks and strict rules surrounding the Primary Account Number (PAN), the way forward becomes much clearer. The single most effective strategy is to stop this sensitive data from ever touching your business environment in the first place.

This isn't about building bigger digital walls around your data. It's about completely redesigning how payment information flows so the PAN never crosses your threshold. When you do this, you dramatically shrink your PCI scope, make compliance far simpler, and create a genuinely secure payment process.

Thankfully, powerful technologies are available that make this possible, finally moving businesses away from flawed methods like 'pause and resume' and into an era of proactive security.

Keeping PANs Out with DTMF Masking

One of the most powerful tools for securing phone payments is Dual-Tone Multi-Frequency (DTMF) masking. You've already used this technology thousands of times—it's the sound each key makes when you dial a phone number.

In a payment context, DTMF masking lets a customer punch their card number directly into their telephone keypad. As they press each key, the tones are captured by a secure payment platform but are completely masked or silenced on the agent's end.

Think of it as a private, secure line between the customer's keypad and the payment gateway. The agent can stay on the call to guide the customer through the process, but they never hear or see the sensitive PAN data. It's an elegant solution that solves several problems at once:

- No Verbal Exposure — The agent never hears the card details, wiping out the risk of internal fraud or accidental exposure.

- Clean Call Recordings — Because the DTMF tones are masked, the call recording is instantly compliant, as it contains zero sensitive cardholder data.

- Reduced PCI Scope — The agent and their entire workstation are removed from PCI scope because they no longer handle the PAN.

This one piece of technology effectively neutralises the highest-risk channel for phone payments: the live conversation between an agent and a customer.

The Power of Tokenization

While DTMF masking stops the PAN at the door, tokenization ensures that even after a payment is processed, you never need to store the raw card number for future use. It's a simple concept, but incredibly powerful.

Imagine you're checking your coat at a theatre. You hand over your valuable coat and get a simple numbered ticket. That ticket is worthless to a thief; they can't wear it or sell it. But for you, it's the key to securely retrieving your coat later.

Tokenization works exactly the same way. When a payment is made, a secure payment provider captures the real PAN and swaps it for a unique, non-sensitive "token." This token is just a randomly generated string of characters that refers back to the original card data, which stays locked away in the payment provider's secure vault.

Tokenization is the process of substituting a sensitive data element with a non-sensitive equivalent, referred to as a token, that has no extrinsic or exploitable meaning or value. This token can be used for future transactions without exposing the original PAN.

The beauty of this system is that your business can store and use these tokens for recurring billing, refunds, or customer lookups without ever handling the actual PAN again. If your systems were ever breached, all the thieves would find is a collection of useless tokens.

A Layered Defence for Total Security

Combining DTMF masking and tokenization creates a powerful, layered security strategy that protects the entire payment lifecycle. The UK sees a massive volume of card transactions, making solid security measures an absolute necessity. While specific statistics on PAN data are not readily available, the sheer scale of card usage highlights the vast amount of sensitive data being handled daily.

Here's how these two technologies work together in a typical contact centre:

- A customer calls to make a payment and is guided by an agent.

- The customer enters their PAN using their phone keypad, while DTMF masking prevents the data from ever reaching the agent or the call recording.

- The secure payment platform sends the encrypted PAN to the payment gateway.

- The gateway processes the transaction and returns a token to your systems—not the PAN.

- Your business stores this safe, reusable token for any future customer interactions.

This modern, de-scoped approach is the gold standard for handling PAN data. It protects your customers, drastically simplifies your PCI DSS obligations, and frees your business from the liability of storing toxic data. To ensure ongoing protection of sensitive financial data like PANs, many organisations use Managed Cybersecurity Services to maintain a strong security posture.

Common Questions About Primary Account Numbers#

Getting your head around the theory of the Primary Account Number (PAN) is one thing. Figuring out how it all works in the real world of your business is something else entirely. We've pulled together some of the most common questions we hear from business owners, contact centre managers, and compliance officers to clear things up.

Is the PAN the Same as the Credit Card Number?

Yes, for all intents and purposes. In everyday conversation, 'credit card number' is what everyone says, but PAN is the official term used by the industry—think payment networks and the PCI Security Standards Council.

It's that unique string of digits, usually 14 to 19 numbers long, stamped right on the front of a payment card. So, when a customer reads out their 'card number', they're giving you their PAN.

What Is the Difference Between a PAN and a Token?

This is a important distinction, and it's at the heart of modern payment security. A PAN is the live, sensitive account number. It's the direct link to a customer's funds and is all that's needed to authorise a transaction. A token, on the other hand, is a secure, non-sensitive stand-in for that number.

Tokenization is a clever process where the original PAN is swapped out for a unique, algorithmically generated value—the token. The magic here is that this token can't be reverse-engineered to reveal the original PAN, making it completely useless to a fraudster if it ever gets stolen.

A PAN is the key to the vault, while a token is a single-use claim ticket. One holds immense value and risk; the other is a secure reference point with no intrinsic worth.

While the token points back to the real PAN stored safely by a payment provider, it's often locked down for use with a specific merchant. This is why tokenization is a cornerstone of any smart strategy for shrinking your PCI scope and tightening security.

Why Is Pause and Resume Not Enough to Protect PANs?

The old 'pause and resume' trick for call recordings is a classic but deeply flawed way to try and protect PAN data. The whole thing relies on perfect execution by both people and technology, which, let's be honest, is a pretty unrealistic expectation in a busy contact centre.

So many things can go wrong:

- Human Error — An agent forgets to hit pause, pauses too late, or resumes too early. A simple mistake is all it takes to capture part of the PAN.

- System Lag — Delays in the recording software can mean sensitive audio is captured even after the agent has hit the pause button.

- Incomplete Protection — This is the biggest flaw. 'Pause and resume' does absolutely nothing to stop the agent from hearing the PAN or seeing it on their screen. The data is still exposed right there in your contact centre.

Modern solutions like DTMF masking take a much better approach by removing the PAN from the agent's environment altogether. The risk is eliminated because the data was never there in the first place.

How Does Protecting the PAN Help with GDPR Compliance?

Under the General Data Protection Regulation (GDPR), a PAN is considered sensitive personal data. If you fail to protect it properly, you're directly violating core principles of the regulation, like 'data protection by design and by default'.

A data breach involving PANs can land you with massive GDPR fines, which are completely separate from any penalties you might face for not meeting PCI DSS rules. By using technologies that de-scope your environment—stopping PANs from ever being stored or processed on your systems—you're showing a serious, proactive commitment to protecting personal data. That proactive stance is a huge part of a strong GDPR compliance posture and proves you take customer privacy seriously.

At Paytia, we eliminate these complexities by ensuring the PAN never enters your business environment. Our secure payment solutions use DTMF masking and tokenization to de-scope your operations from PCI DSS, protecting your customers and simplifying your compliance. Discover how Paytia can secure your payments today.

Related reading#

- Pillar guide: Card Not Present (CNP) Explained: Risks and How to Reduce

- How AI Is Transforming Secure Payment Services

- Payment Validation: Complete Guide for Businesses

- 3DS2 Liability Shift: How Authentication Works

- Are Payment Links Safe? What to Check Before You Pay

Curious how Paytia fits in? Have a quick chat with us — we'll show you in 15 minutes whether we're a fit.