That little three or four-digit number on your credit card? It’s called a credit card security code, and it’s one of the simplest yet most effective tools for keeping your money safe. When you buy something online or over the phone, merchants ask for this code to prove that you actually have the card in your hand.

Think of it as a quick, digital check-in. It confirms you’re the legitimate cardholder, not just someone who found a lost receipt or stole a card number from a database. This simple step is a critical first line of defence against would-be fraudsters.

Key takeaways

- The credit card security code (CVV/CVC/CSC) proves the cardholder has the physical card during a transaction.

- It's different from your PIN — the security code is for card-not-present transactions, not in-store purchases.

- Businesses collecting this code by phone must ensure it's never recorded or accessible to agents.

- Under PCI DSS, storing this code after authorisation is explicitly prohibited, even if encrypted.

Your Guide to Card Security Codes#

It’s helpful to think of the difference between your main card number and your security code like this. The 16-digit number is your public address, telling the merchant where to send the bill. The security code, on the other hand, is like a one-time-use key to your front door. It’s a secret you share only at the moment you’re making a purchase.

This distinction becomes absolutely vital in what the industry calls "card-not-present" (CNP) transactions. Whenever you aren't physically tapping your card or inserting its chip, the risk of fraud shoots up. That tiny security code is what bridges the trust gap.

The Different Names for One Important Number

You’ve probably seen a few different acronyms for this code, which can get confusing. While they all do the exact same job, each major card network has its own preferred term:

- CVV or CVV2 — Stands for Card Verification Value, the term used by Visa.

- CVC or CVC2 — This is the Card Verification Code, which you’ll see associated with Mastercard.

- CID — Short for Card Identification Number, used by American Express (and uniquely placed on the front of the card).

- CSC — A more generic term, Card Security Code, that you might see used.

Here’s the clever bit: this code is only printed on the card. It's not stored on the magnetic stripe and it's not embedded in the EMV chip. This is intentional. It means that even if a criminal manages to "skim" your card data from a dodgy payment terminal, they still won't have the security code. That stops them from using those stolen details for online shopping sprees.

Your Guide to Finding the Security Code

To make it easy to find the code on your own cards, here's a quick reference guide.

| Card Network | Code Name | Number of Digits | Location on Card |

|---|---|---|---|

| Visa | CVV/CVV2 | 3 | On the back, in the signature strip |

| Mastercard | CVC/CVC2 | 3 | On the back, in the signature strip |

| American Express | CID | 4 | On the front, above the card number |

| Discover | CID | 3 | On the back, in the signature strip |

Knowing where to look and what this code does is a great first step towards protecting your payment details. If you're keen to explore this topic further, you can learn more about what is the security code on a card and its vital role in modern transactions.

The Surprising UK Origins of the Security Code#

It’s easy to think of that little number on the back of your card as a modern security feature, born from the internet age. But its story actually begins much earlier, in an era of mail-order catalogues and landline phone calls. The entire concept was invented right here in the UK. It solved a problem that’s still a huge challenge for businesses: how to safely take a payment when you can’t see the customer or their card.

Back in 1995, a man named Michael Stone, who worked for Equifax, came up with the idea. He created it specifically to secure transactions for mail-order companies and telephone sales — the original “card-not-present” fraud hotspots. His first version wasn't the simple three or four digits we see today; it was a much more complex 11-character alphanumeric code.

From Complex Code to Simple Standard

The first real-world test of this new security system involved Littlewoods Home Shopping and NatWest Bank. The trial was a success, and it didn't take long for the UK's payment authority, the Association for Payment Clearing Services (APACS), to see its potential for stopping the rising tide of fraud.

APACS took the core idea and simplified it, creating the three-digit credit card security code standard that became the global norm. This backstory is more than just a bit of trivia; it shows that the security code was never an afterthought.

It was purpose-built from day one to solve a single, critical problem: proving that the person making a remote purchase actually has the physical card in their hands. That simple principle is still its greatest strength.

When you understand where it came from, you see the security code for what it is—not just a random number, but a clever defence mechanism born out of necessity. The challenges of taking secure payments over the phone in the 90s directly paved the way for protecting the billions of online and contact centre transactions we see every day. This British progress truly became a cornerstone of global payment security, a journey you can explore by reading more about the history of UK payment milestones.

Comparing options? Book a 15-minute demo — we'll show you a live capture and quote a real number for your call volume.

How Your Security Code Stops Fraudsters#

The real magic of the security code happens when a payment is made remotely. In any situation where your customer isn't physically there to tap or insert their card, that little three or four-digit number becomes your most important defence against fraud.

Think of it as a digital handshake. A fraudster might buy a list of stolen credit card numbers and expiry dates from a data breach—sadly, this information is all too common on the dark web. But without the security code, those stolen details are often completely useless for making online or phone purchases.

That's because the security code is deliberately kept separate from all other card data. It's printed on the physical card but isn't stored in the magnetic stripe or the chip. Crucially, businesses are strictly forbidden from ever storing it after a transaction is authorised. This single rule makes huge databases of stolen card numbers far less of a goldmine for criminals.

The Rise of Card-Not-Present Fraud

This simple security feature is more vital today than ever before. The single biggest threat facing UK businesses is card-not-present (CNP) fraud, which is the official term for any transaction made online, by mail order, or over the phone.

And the scale of the problem is staggering. In 2022, total card fraud losses in the UK hit £556.3 million. A massive 81% of that—or £396 million—came directly from CNP fraud, where getting the security code is often the final step for a criminal. These UK finance fraud statistics highlight a huge vulnerability for any business that takes payments remotely, especially contact centres.

The security code acts as a firewall. It separates the static data that gets stolen so often (card number, expiry date) from the proof that someone actually has the card in their hand. It’s the difference between knowing someone’s address and having the key to their front door.

Why It Is Your Last Line of Defence

For a fraudster, getting that security code is the final piece of the puzzle. Once they have it, they can sail past the main security checks on most e-commerce and telephone payment systems. This is why protecting the CVV during the payment process itself is an absolute priority.

If a criminal cons a customer into revealing it through a phishing scam, or if an employee handles it insecurely over the phone, that protective barrier is completely gone. You can learn more about these risks in our guide on what card-not-present fraud means for your business. Getting to grips with this is the first step toward building a payment process that is genuinely secure.

The Golden Rule of Handling Security Codes#

When it comes to handling customer payments, there’s one non-negotiable, absolute golden rule for the credit card security code. This isn't just a recommended approach; it's a strict mandate from the Payment Card Industry Data Security Standard (PCI DSS), the global framework that dictates how every business must protect cardholder data.

Put simply, the rule is this: you are strictly forbidden from storing the security code (CVV, CVC, or CID) after a transaction has been authorised.

That means nowhere. Not on a piece of paper, not in a spreadsheet, not in your CRM, and certainly not in any database. The moment that payment gets the green light, that three or four-digit code must be gone for good.

This isn't just bureaucratic red tape. It's the very core of what makes the security code such a powerful weapon against fraud. By making it illegal for merchants to store this code, the PCI DSS limits the damage of a breach. Even if a criminal hacks a company’s database and makes off with millions of card numbers, they still won’t have the one piece of the puzzle they need. Without the security code they can't use those cards online or over the phone.

Why This Rule Is So Critical

Think about it. The entire security model is built to make stolen card databases less valuable. A list of card numbers and expiry dates is certainly a threat, but a list that also includes the security codes is a fraud catastrophe just waiting to happen. The "no storage" rule effectively pulls the rug out from under fraudsters by devaluing the data they work so hard to steal.

PCI DSS Requirement 3.2.2 puts it in no uncertain terms — "Do not store the card verification code or value (three- or four-digit number printed on the front or back of a payment card used to verify card-not-present transactions) after authorisation."

This single requirement is what turns the security code into a genuine defence. It stops it from being just another piece of static, stealable information. The code can't be hoarded in a stolen database and used later — it only works at the moment the customer has the card in their hands.

Where Businesses Often Go Wrong

For businesses with contact centres, this rule presents a unique and constant challenge. The pressure of taking payments over the phone — with queues building and customers waiting — can easily lead to accidental and highly dangerous compliance breaches.

Here’s a look at some of the most common mistakes we see:

- The Sticky Note Scramble — An agent quickly jots down the security code on a sticky note to type it into the payment system. Then they forget to shred it immediately.

- Accidental Call Recordings — Standard call recordings capture the customer saying their security code out loud, storing it in audio files that are often kept for years for quality assurance purposes.

- CRM and Note-Taking Traps — Staff might type the full card details, security code included, into an order notes field in their customer management software out of habit.

Each of these scenarios creates a serious security vulnerability and puts your business in direct violation of PCI DSS rules. Understanding this golden rule isn't just about avoiding hefty fines; it's about protecting your customers and preserving the trust they place in your business every time they pay.

Security Code Handling Do's and Don'ts

To make this crystal clear, here’s a simple breakdown of what is and isn't allowed when your team handles security codes.

| Action | Compliant Practice (Do) | Non-Compliant Practice (Don't) |

|---|---|---|

| Data Entry | Enter the code directly into a validated, PCI-compliant payment system that immediately uses and discards it after authorisation. | Write the code down on paper, in a text file, or on a whiteboard, even for a few seconds. |

| Verbal Payments | Use a secure system (like DTMF masking) that prevents the agent from hearing or seeing the code and stops it from being recorded. | Allow the customer to read their security code out loud on a recorded phone line. |

| Digital Notes | Ensure no field in your CRM, order system, or internal chat allows for the security code to be typed or saved. | Type the full card number, expiry, and security code into a "notes" or "comments" field in any software. |

| Data Storage | Ensure your systems are configured to reject or immediately delete the security code post-authorisation. | Store the security code in any database, log file, or call recording archive. |

Following these "Do's" isn't just about compliance; it's about building a secure foundation for your payment processes. The "Don'ts" aren't just bad habits—they are critical security risks that expose your business and your customers to fraud.

Why Stolen Security Codes Are a Goldmine for Criminals#

To really grasp why a simple three or four-digit credit card security code is so valuable to a criminal, you have to think bigger. The value isn't in a single fraudulent purchase. Stolen card details aren't just used once and then discarded. They’re part of a massive, well-oiled illegal economy on the dark web where data is bought, sold, and traded like any other commodity. This isn't some distant threat; it's a bustling marketplace operating 24/7.

The moment your card number, expiry date, and security code are out in the wild, they become a product. Cybercriminals package this information into lists and sell them off for shockingly small amounts to fraudsters all over the world. For the buyers, it's a low-risk, high-reward business model that powers everything from dodgy online shopping sprees to full-scale identity theft.

The Dark Web Marketplace for Stolen UK Cards

This black market is a particularly big problem for anyone with a UK bank card. One eye-opening piece of research sifted through a database of 6 million stolen cards and found that Britain was the most targeted country in Europe. The study flagged a staggering 164,143 UK payment card details up for sale.

Even more worrying was the price. The average cost for a set of UK card details was just £4.61—far cheaper than the global average. This makes UK card data a bargain for criminals and directly fuels card-not-present fraud, which hit the UK for £396 million in 2022 alone. You can read more about the UK's vulnerability to card fraud to see the full picture.

The data becomes exponentially more valuable when the security code is part of the package. A card number on its own is difficult to use, but adding the CVV instantly unlocks it for online and phone-based fraud.

A stolen credit card security code is the key that turns a useless string of numbers into instant cash for a fraudster. It completes the package they need to bypass the most common online security checks.

How Your Data Ends Up for Sale

So, how do these security codes and card details get swiped in the first place? Criminals have a whole playbook of tricks they use to get their hands on this information, ensuring a steady supply for the dark web economy.

- Phishing Scams — These are the classic bait-and-switch emails or texts that lure you to a fake website. The fake site looks just like your bank or a favourite online shop and tricks you into typing in your details.

- Malware and Skimmers — Nasty software hiding on your computer can log everything you type, including card details. In the physical world, criminals attach "skimming" devices to ATMs or payment terminals to clone your card when you use it.

- Major Data Breaches — Hackers go after the big fish, targeting large companies to steal massive databases filled with millions of customer payment details in one fell swoop.

Once a credit card security code is exposed through any of these routes, it’s almost guaranteed to be used for fraud. That's precisely why being proactive about security is so incredibly important.

Modern Solutions for Securing Payment Data#

After seeing how easily a stolen credit card security code can fuel fraud, it's pretty clear that old-school ways of handling payments just don't cut it anymore. The risk of an agent seeing or hearing sensitive details—or having them captured on a call recording—is simply too high. Thankfully, modern security technology gives us a much safer path forward.

These solutions are built on a simple but powerful idea: sensitive payment data should never even enter your business environment. It’s all about creating a secure bubble around the transaction, shielding your organisation from ever having to touch the data itself.

How Technology Shields Sensitive Codes

Two key pieces of technology make this happen: DTMF suppression and channel separation. They might sound a bit technical, but the concepts are actually quite straightforward.

Think of DTMF suppression as a smart 'digital mute button'. When a customer taps their security code into their telephone keypad, this technology cleverly masks the tones. Your agent can stay on the line to help, but all they hear is a flat, monotonous sound—not the distinct beeps that correspond to the numbers. The system captures the details securely without a human ever hearing them or a call recording ever storing them.

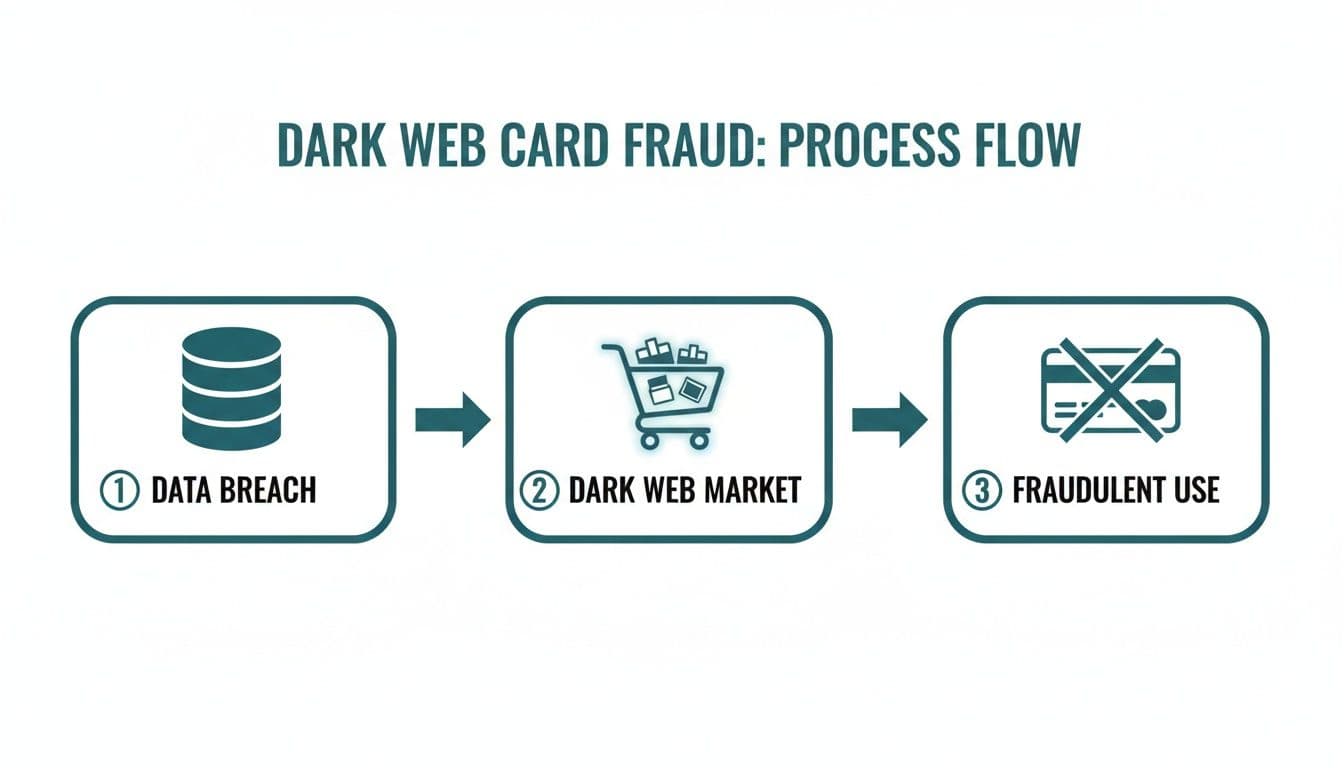

This process is designed to break the chain of fraud, which often starts with a single data breach and escalates quickly, as this diagram shows.

As you can see, once card details land on the dark web, they can be used for widespread fraudulent activity. Preventing that initial theft is everything.

Creating a Secure Payment Tunnel

Next up is channel separation, which you can picture as a secure, invisible tunnel. When it’s time to pay, this tech redirects the sensitive part of the conversation—like entering the security code or the long card number—straight from the customer to the payment processor.

The payment data completely bypasses your agents, your call recordings, and all your computer systems. It travels through its own encrypted channel, never once touching your network. This approach delivers some massive wins:

- Drastically Reduced PCI Scope — Because sensitive data never enters your environment, your PCI DSS compliance burden can shrink by as much as 90-95%.

- Elimination of Insider Threat — Agents can't see, hear, or access card details, which removes the risk of accidental exposure or internal fraud.

- Improved Customer Trust — Customers feel more confident knowing they aren't reading their private information aloud to a person.

The real major improvement here is that your business can process a payment without ever possessing the sensitive data. This neatly sidesteps the PCI DSS rule against storing security codes and protects you from the fallout of a data breach.

By bringing these solutions on board, you’re not just ticking a compliance box. You're rebuilding your payment process to be secure by design. These techniques are often paired with other powerful tools. To explore another layer of protection, you can learn more about what tokenization is in payments and how it adds yet another safeguard for customer data.

CVV, CVC, CCV, and CSC: what each term means#

If you've ever looked at a payment form and wondered whether CVV, CVC, CCV, and CSC are all the same thing — yes, they are. They're different names for the same short security code printed on your card. Here's a plain-English breakdown of each term so you know exactly what any checkout page is asking for.

Why so many acronyms? The security code was introduced in the late 1990s, and each card network trademarked its own name. Visa went with CVV (Card Verification Value). Mastercard picked CVC (Card Verification Code). American Express and Discover call theirs the CID (Card Identification Number). The wider industry term is CSC (Card Security Code). Nobody ever agreed to standardise them, so all the names stuck.

What is a CVV?

A CVV is the three or four-digit security code printed on a credit or debit card, used to prove the cardholder physically has the card during an online or phone payment.

CVV stands for Card Verification Value — that's Visa's original name for the code, and it's the one most people use. On Visa, Mastercard, and most other cards, you'll find the CVV printed on the back, on or next to the signature strip. On American Express cards, it's four digits printed on the front.

The CVV exists because the 16-digit card number and expiry date aren't enough on their own. Those details often sit in databases, on old receipts, or inside email confirmations. The CVV doesn't — it's only ever printed on the physical card, and under PCI DSS it's never allowed to be stored after a payment is authorised. That's what makes it a genuine proof that you have the card in your hand.

CVC meaning: what the acronym actually means

CVC means Card Verification Code. It's Mastercard's name for the three-digit security code printed on the back of the card, and it works exactly like a Visa CVV.

If you've got a Mastercard-branded debit or credit card, the three digits next to the signature strip are your CVC. You'll sometimes see it written as CVC2 — the "2" just means it's the printed version, not the older CVC1 that used to be encoded in the magnetic stripe. For a checkout page it doesn't matter which label the form uses. If it asks for CVV and your card says CVC, type the same three digits. The payment system treats them as the same field.

The reason Mastercard picked a different name from Visa is pure branding — both networks wanted their own trademarked term when the code was introduced in the 1990s. The job it does is identical: it proves you physically have the card during a card-not-present payment.

What is a CVC number?

A CVC number is the three-digit Card Verification Code printed on the back of a Mastercard, used to confirm the card is physically present during online or phone payments.

You'll find the CVC on the signature strip, usually printed in a slightly smaller font after the last four digits of the card number. It isn't embossed, it isn't raised, and it isn't part of the main 16-digit number. That's deliberate — the idea is that someone skimming card details from a receipt or an old database won't have the CVC, so they can't complete a card-not-present transaction.

If you're a Mastercard holder paying online, the CVC is what the form's asking for when it says "security code", "CVV", "CVC", or "3 digits on back". It's all the same number. And if a merchant over the phone asks you to read it out, that's a red flag — legitimate PCI-compliant setups like Paytia let you key it yourself so it never touches the agent.

CSC meaning: what card security code really is

CSC stands for Card Security Code. It's the generic industry term for the three or four-digit code printed on a payment card, covering Visa's CVV, Mastercard's CVC, and Amex's CID.

You'll see CSC used in documentation, PCI DSS guidance, and on payment forms that don't want to pick a network-specific name. It's the neutral label. If your payment provider writes "CSC" on a page, they just mean "whatever the security code is on the card you're using, type it here." Some UK banks and older point-of-sale systems use CSC in their own paperwork too.

For cardholders, CSC is the term to remember if you want one name that always applies. For merchants handling payments over the phone, CSC is the data field that PCI DSS bans you from storing after a transaction is authorised. That means no call recordings, no CRM notes, no "just for the refund later". Once the payment is through, the code is gone.

CCV meaning: is CCV actually a real thing?

CCV is an informal spelling of the card security code — usually short for "Card Code Verification" or "Credit Card Verification". It isn't an official network term, but it refers to the same three digits.

You'll see CCV mostly on US checkout pages and in older merchant documentation. It got popular because some people misremembered CVV as CCV, and the spelling stuck. Visa, Mastercard, and Amex don't use CCV in any of their official literature — they use CVV, CVC, and CID respectively. But if a payment form asks you for your "CCV", it means the same thing: the three digits on the back of your card, or the four on the front of an Amex.

If you're building a checkout page, use CVV or "security code" rather than CCV. It's clearer for customers and matches what card networks actually call it. CCV isn't wrong, it's just unofficial.

CVV code meaning: what it is and why it matters

The CVV code meaning is straightforward. It's the short security code printed on your card that proves you physically have the card when you're paying without presenting it in person.

"CVV code" is a bit redundant — the V already stands for Value, so "CVV code" technically means "Card Verification Value code". But the phrase has stuck because people want to make clear they mean the little number, not the big one. If you see "enter your CVV code" on a checkout page, enter the three digits on the back of your Visa or Mastercard, or the four on the front of your American Express.

Why does it matter? Because it's one of the few pieces of card data that isn't in every database breach. Card numbers and expiry dates leak all the time. The CVV is supposed to be locked to the physical card, so even if a fraudster has your main card details, a CVV-protected checkout will block them. That's the whole point, and it's why merchants handling phone payments need tools that capture it without exposing it to agents or call recordings.

What contact centres need to know about CVV#

Three rules matter operationally for any contact centre taking card payments over the phone.

You cannot store the CVV after authorisation. The PCI DSS prohibits storing the CVV — also called the "sensitive authentication data" or SAD — after the transaction is authorised. This applies whether the storage is in a database, a CRM note, a call recording, or a paper notepad on an agent's desk. Storage of CVV is one of the most common findings in mid-cycle PCI audits.

Call recordings are storage. A call recording that captures an agent reading back card details, or a customer reading them aloud, is storing CVV in violation of the PCI rules. This is one of the structural drivers behind DTMF masking. The customer keys the digits on their handset, the tones are intercepted before they hit the agent's audio leg, and the recording captures silence in place of card data.

The CVV is a check, not a guarantee. A correct CVV match raises the probability that the caller has the physical card; it does not eliminate card-not-present fraud. Issuers frequently authorise CVV-mismatched transactions with a soft decline that the merchant can override. Treat CVV match as one signal in a fraud-screen stack, not a single point of truth.

For the broader compliance frame around CVV handling, see our overview of PCI DSS v4.0.1 for contact centres. If your contact centre is currently handling CVV by reading-back-and-keying, talk to a Paytia specialist. The PCI conversation usually starts there.

Frequently asked questions#

What does CVV stand for?

CVV stands for Card Verification Value. It's the three-digit code printed on the back of most Visa-branded cards, on the signature panel. American Express calls its equivalent "CID" and prints it as four digits on the front of the card.

What's the difference between CVV and CVV2?

CVV1 is encoded in the magnetic stripe and is not the value consumers see. CVV2 is the printed version — the three digits on the back of the card. When people refer to "the CVV," they almost always mean CVV2.

Is CVV the same as CVC?

Functionally yes. CVV is Visa's term; CVC ("Card Verification Code") is Mastercard's term. Both refer to the same three-digit security code printed on the card.

Where do I find the CVV on my card?

On Visa and Mastercard cards, the CVV is the three-digit number on the back, near the signature strip. On American Express, the four-digit CID is printed on the front of the card, above the embossed card number.

Why is the CVV not on the magnetic stripe?

Keeping the CVV2 off the stripe means a card that's been skimmed (where the stripe is copied) cannot be used for online or phone purchases that require the printed CVV. It's a deliberate fraud-prevention design.

Can a merchant store my CVV?

No. The PCI Data Security Standard prohibits merchants from storing the CVV after the transaction is authorised. This applies to databases, CRM notes, call recordings, and any other form of storage.

Does a correct CVV mean the transaction is safe?

Not on its own. A correct CVV raises the probability that the caller has the physical card, but it doesn't rule out card-not-present fraud, account takeover, or synthetic identity scenarios. Issuers and merchants treat CVV match as one signal among several.

Why does the contact-centre agent ask for the CVV every time?

Because PCI rules don't allow the CVV to be stored. A merchant has to capture it fresh on each transaction, even for repeat customers, even where other card details are stored.

What's the difference between CVV and a PIN?

A PIN is your secret personal identification number — used at ATMs and in-person card-present transactions. The CVV is a static printed value on the card that the merchant can verify in card-not-present transactions. PINs are confidential to the cardholder; CVVs are printed on the card itself.

Can a fraudster guess a CVV?

Mathematically there are 1,000 possible three-digit combinations, so brute-forcing a CVV is feasible against a single transaction. Issuer fraud systems detect repeated mismatched-CVV attempts and lock the card; this is the standard defence against guessing.

What is CV2?

CV2 is another term for CVV2 — the same three-digit printed code. It's used most often in UK and EU acquirer documentation.

What does CCV mean?

CCV is a misspelling of CVV that has become common enough to appear in search queries. It refers to the same three-digit security code on the back of the card.

Secure your customer payments and simplify your compliance with Paytia. Discover our solutions for protecting payment data over the phone and other channels.

Stop storing the CVV — let Paytia handle it

Paytia captures card details directly from your customer's phone keypad, without ever exposing CVV, PAN, or expiry date to your agents or your systems. Zero card data in your environment.

Related reading#

- Pillar guide: Card Not Present (CNP) Explained: Risks and How to Reduce

- What Is a PAN? Understanding Primary Account Numbers

- How AI Is Transforming Secure Payment Services

- Payment Validation: Complete Guide for Businesses

- 3DS2 Liability Shift: How Authentication Works

Comparing options? Book a 15-minute demo — we'll show you a live capture and quote a real number for your call volume.